While Oil and Gas (O&G) operations are responsible for roughly 15 percent of global energy-related GHG emissions, some energy companies have pledged the role of natural gas (NG) as a transitional fuel. At the same time, NG energy use is increasing globally, and shale-gas extraction is booming at an unprecedented rate. One factor that is often overlooked is the methane emissions across the NG value chain.

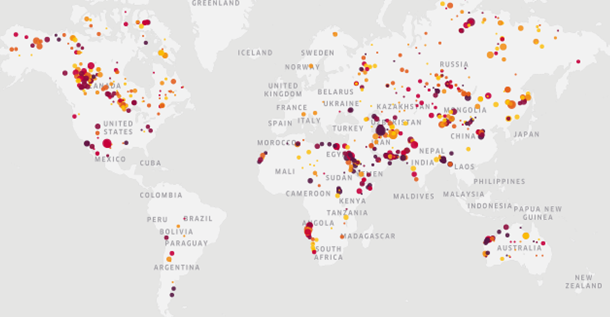

Although it persists in the atmosphere for less time, methane has a Global Warming Potential (GWP) 28 times larger than carbon dioxide (CO2) over a 100-year period. There are concerns over the NG projected role as a ‘cleaner’ fossil fuel option, mainly driven by the increasing awareness of the methane emissions related to the NG infrastructure. Exhibit 1 demonstrates key point source emissions of methane from O&G production.

Exhibit 1: Methane Emissions Point Sources[i]

Methane: A Growing Risk

Methane is increasingly facing regulatory requirements and tighter controls. In October 2020, the European Commission adopted a new strategy to reduce methane emissions, including significant actions in the energy sector to improve the measurement, reporting and mitigation of methane emissions. In August 2020, the US EPA rescinded regulations to mitigate methane emissions associated with the NG sector, ending the 2016 rule that required companies to have systems to detect and repair leaks from wells, pipelines and storage tanks. However, the future Biden administration could potentially move quickly in reversing this rollback.

Methane Management Best Practices

The largest sources of methane, the main constituent of NG, are fugitive emissions (unintentional leaks) followed by vented emissions (routine releases due to equipment design or operational practices). There is no single solution to meet this challenge globally. However, according to the O&G Industry in Energy Transitions report by the International Energy Agency (IEA), reducing fugitive emissions is the single most important and cost-effective way for the industry to bring down these emissions.

Methane emissions contribute towards a varying proportion of a company’s total GHG footprint (between 2-73%[ii]), yet the management of these emissions and targeted reductions vary greatly. Mitigating methane emissions require specific measures, especially given the range of operational emissions, demonstrating that best practice management is not employed across the board.

In 2018, the Oil and Gas Climate Initiative (OGCI) set a strong target to help its members, including many oil majors, reduce their average methane intensity to 0.2% by 2025[iii]. This ambitious initiative shows that cutting methane emissions is a key ESG issue across the industry’s operations. Exhibit 2 (below) demonstrates some O&G producers with ambitious plans to reduce methane emissions and their alignment with best practices.

| Company | Methane Commitment | Alignment with Ambitious Reduction Target | Contribution of Carbon Footprint | NG Production estimates (2019) |

| EQT Corp[iv] | Reduce methane emissions across the NG value chain to 1% by 2025 | Not aligned | 72.7% | 95% |

| EOG Resources[v] | Reduce methane emissions percentage to 0.06% by 2025 | Better than best Practice | 22.7% | 23% |

| Shell[vi] | Maintain methane emissions intensity below 0.2% by 2025 | Aligned | 5% | 49% |

| BP[vii] | Achieve a methane intensity of 0.2% | Aligned | 6.5% | 41% |

| Exxon[viii] | Reduce methane emissions by 15 percent by 2020, compared with 2016. Support Methane Guiding Principles | Not aligned | 5.6% | 38% |

| Gazprom[ix] | Reduce methane emissions into the atmosphere (during repair works of gas transmission system). Participates in Methane Guiding Principles | Not aligned | 28% | 89% |

| Rosneft | Joined the international initiative ‘Methane Guiding Principles’ Round Table. | Not aligned | 0.24% | 19% |

| Lukoil[x] | Demonstrate reduced emissions but no target | Not aligned | 2.6% | 24% |

| Equinor[xi] | Ensuring no routine flaring and near-zero methane emissions intensity by 2030 | Aligned | Contribution not reported | 48% |

| Petrobras[xii] | Reducing methane emissions intensity by 30%-50% in exploration and production by 2025 | Aligned | 7.5% | 13% |

| Repsol[xiii] | Reduction target aligned to OGCI metric | Aligned | Contribution not reported | 64% |

| Chevron[xiv] | Reduce intensity by 20-25% by 2023 based on 2016 performance | Not aligned but a member of OGCI | 6.7% | 38% |

| Eni[xv] | Reduce in line with OGCI | Aligned | Contribution not reported | 46% |

| Total[xvi] | Reduce in line with OGCI | Aligned | 5% | 41% |

| Occidental[xvii] | Reduce in line with OGCI | Aligned | 1.7% | 26% |

Exhibit 2: O&G Methane Reduction Commitments

Orphan and inactive O&G wells, a growing concern

Similarly, orphan or abandoned wells, or pipelines or other related facilities that no longer have a legal or financial owner, are becoming a growing concern in North America in recent years, mostly due to their associated environmental risks. Although the US EPA estimates that abandoned O&G wells appear to be a significant source of methane emissions to the atmosphere, this problem’s magnitude is largely unknown as little empirical data is available. Defunct companies are typically not liable for decommissioning or cleaning-up costs. As such, these wells can leak methane for many years or even decades before any potential state-level or federal-level remediation intervention.

Some studies have concluded that the cumulative emissions from orphan wells may be significantly larger than the cumulative leakage associated with O&G production. The US EPA also estimated that there are over 3.2 million orphan O&G wells in the US, which collectively emitted 281 kilotons of methane in 2018, the equivalent to the emissions derived from more than 1.5 million passenger automotive vehicles.

ESG Impact

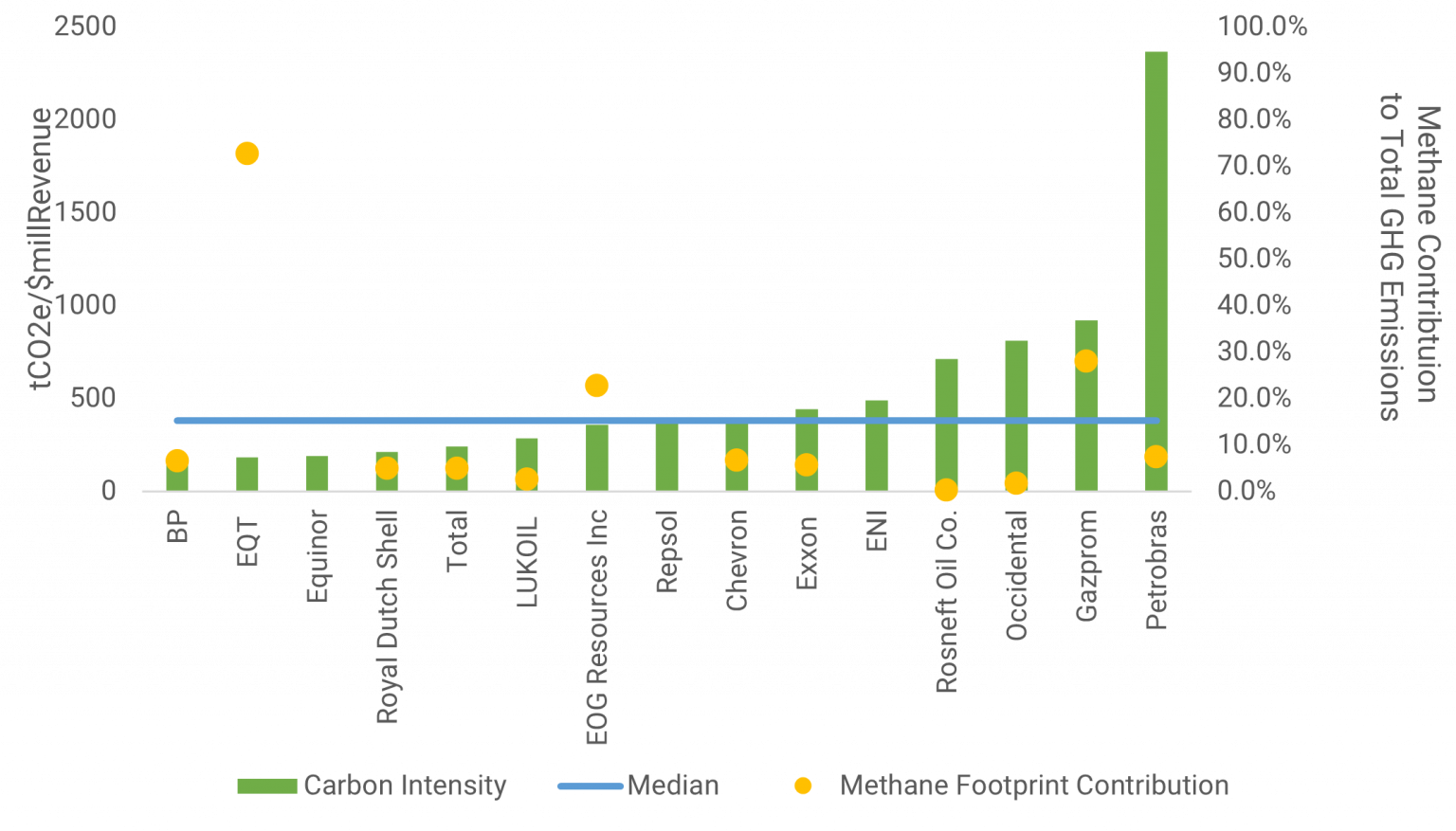

Overall, compared to the industry’s average, those committed to the OGCI’s methane reduction target typically face low carbon-related risks and intensity relating to their operations, albeit with exceptions. Furthermore, they have more progressive carbon reduction targets than their industry peers and already perform well against the target, with lower methane contribution to overall GHG footprints. Also, the larger integrated O&G companies within this group have, on average, lower contributory methane emissions and lower overall carbon intensity against the median.

Those with lower risk to “Carbon – Own Operations”, a material ESG issue (MEI) in Sustainalytics ESG Risk Rating framework, are those with targets aligned to the methane intensity target. However, there is one outlier, EOG has a better than best practice target but higher risks relating to Carbon – Own Operations than others in this analysis. Exhibit 3 (below) compares the operational carbon performance of some O&G producers with ambitious plans to reduce methane emissions.

Exhibit 3: Carbon Performance of “Best Practice” Companies

Learn more about how Sustainalytics’ ESG Risk Ratings enable investors to understand how companies are exposed to specific MEIs and how well companies are managing these issues.

Sources:

[i] European Space Agency, Mapping methane emissions on a global scale

https://www.esa.int/Applications/Observing_the_Earth/Copernicus/Sentinel-5P/Mapping_methane_emissions_on_a_global_scale

[ii] EQT; Climate & GHG Emissions

https://esg.eqt.com/environmental/climate-and-ghg-emissions/

[iii] OGCI; Reducing Methane Emissions

https://oilandgasclimateinitiative.com/action-and-engagement/reducing-methane-emissions/#methane-target

[iv] ESG; Climate & GHG Emissions

https://esg.eqt.com/environmental/climate-and-ghg-emissions/

[v] EOG 2019 Sustainability Report

https://www.eogresources.com/wp-content/uploads/2020/09/EOG_2019_Sustainability_Report.pdf

[vi] Royal DutchShell 2019 Sustainability Report

https://reports.shell.com/sustainability-report/2019/sustainable-energy-future/managing-greenhouse-gas-emissions/methane-emissions.html

[vii] BP; Reducing emissions in our operations

https://www.bp.com/en/global/corporate/sustainability/climate-change/reducing-emissions-in-our-operations.html

[viii] ExxonMobil Sustainability Report – Managing climate change risks

https://corporate.exxonmobil.com/Community-engagement/Sustainability-Report/Environment/Managing-climate-change-risks#Methaneemissions

[ix] Gazprom 2019 Sustainability Report

https://www.gazprom.com/f/posts/72/802627/gazprom-environmental-report-2019-en.pdf

[x] Lukoil 2019 CSR Report

https://csr2019.lukoil.com/climate-change/goals-and-indicators

[xi] Equinor; Equnior Climate

https://www.equinor.com/en/how-and-why/climate.html

[xii] Petrobas 2019 Sustainability Report

https://petrobras.com.br/en/society-and-environment/sustainability-report/

[xiii] Repsol; Methan Policy Recommendations

https://www.repsol.com/imagenes/global/en/methane_policy_recommendations_european_union_tcm14-192770.pdf

[xiv] Chevron 2019 Corporate Sustainability Report

https://www.chevron.com/-/media/shared-media/documents/2019-corporate-sustainability-report.pdf

[xv] ENI 2019 Sustainability Performance

https://www.eni.com/assets/documents/eng/just-transition/2019/Eni-for-2019-Sustainability-performance.pdf

[xvi] Total Climate 2019

https://www.total.com/sites/g/files/nytnzq111/files/atoms/files/total_rapport_climat_2019_en.pdf#page=30

[xvii] Occidental 2019 Climate Report

https://www.oxy.com/Sustainability/overview/SiteAssets/Pages/Social-Responsibility-at-Oxy/Assets/Occidental-Climate-Report-2019.pdf

Recent Content

Six Best Practices Followed by Industries Leading the Low Carbon Transition

In this article, we take a closer look at the leading industries under the Morningstar Sustainalytics Low Carbon Transition Rating (LCTR) and examine the best practices that have allowed them to emerge as leaders in managing their climate risk.

-5-key-questions-answered-about-company-readiness-and-investor-risk.tmb-thumbnl_rc.jpg?Culture=en&sfvrsn=ee2857a6_2 "Navigating the EU Regulation on Deforestation-Free Products (EUDR): 5 Key Questions Answered About Company Readiness and Investor Risk")

Navigating the EU Regulation on Deforestation-Free Products: 5 Key EUDR Questions Answered About Company Readiness and Investor Risk

The EUDR comes into effect in December 2024, marking an important step in tackling deforestation. In this article, we answer five key questions who the EUDR applies to, how companies are meeting the requirements, and the risks non-compliance poses to both companies and investors