Water – An Increasing Operational Risk

The 20th century was the era of cheap, safe, reliable water supply. Although water plays a vital role in the production and availability of almost all products and services, many consumers understate its contribution to our daily lives. Indeed, in the 21st century, water has been, most of the time, an abundant, cheap, and safe resource in developed countries.1

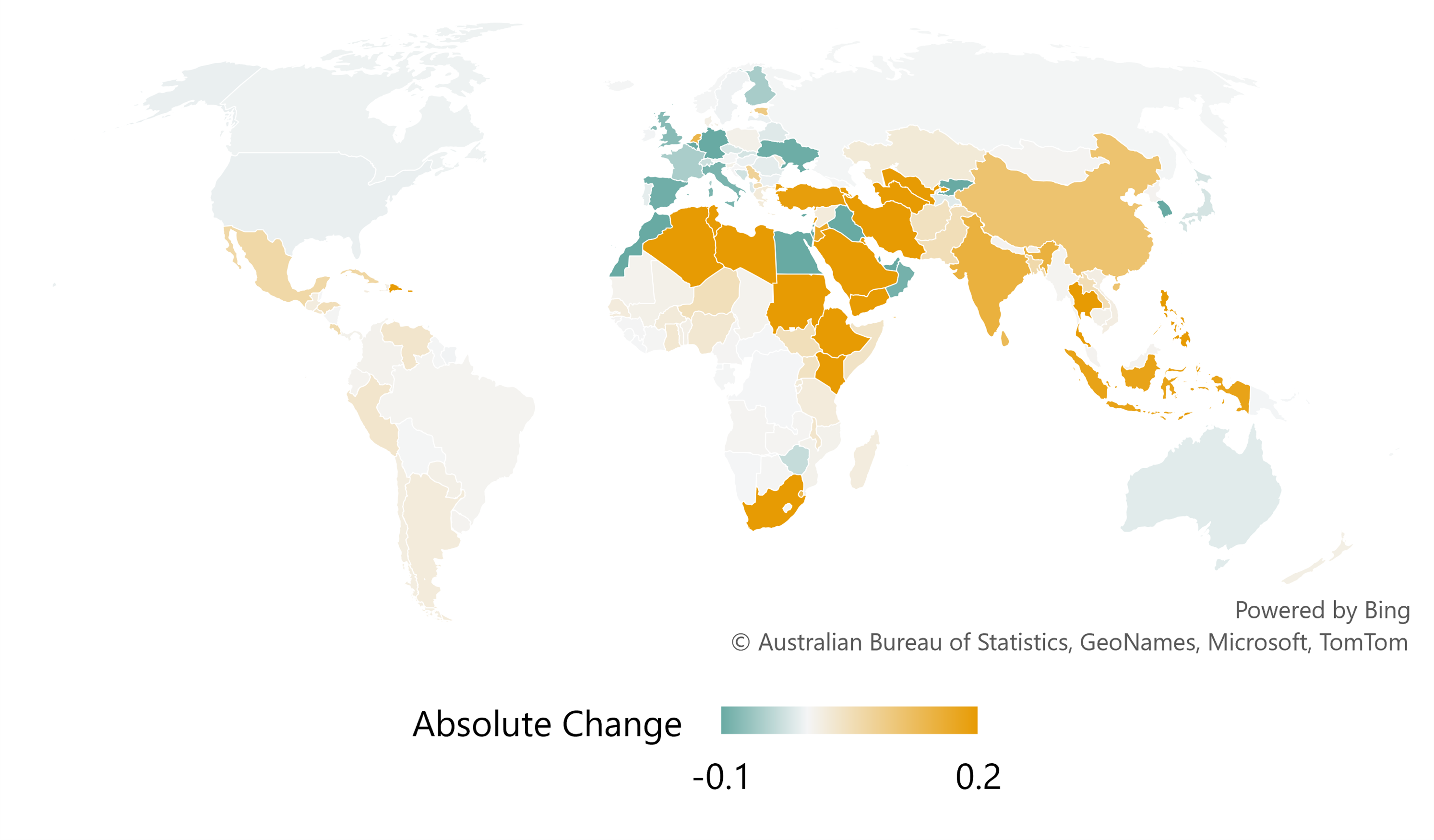

Nevertheless, in most regions of the world, especially those with large populations, both the availability and quality of freshwater are deteriorating (see Exhibit 1). Society contends with over-extraction, poor management of resources, and the continuing loss of wetlands that are directly responsible for biodiversity loss. As a result of human exploitation and mismanagement of water resources, water use limits are already being exceeded.

Exhibit 1: Forecasted Absolute Change in Water Stress - 2002 to 2030

*2002 to 2017 and water withdrawals based on Aquastat data, with forward demand forecasts based on IFPRI Agriculture growth, IMF country GDP forecasts, ourworldindata.org Population Growth.2

*2002 to 2017 and water withdrawals based on Aquastat data, with forward demand forecasts based on IFPRI Agriculture growth, IMF country GDP forecasts, ourworldindata.org Population Growth.2

Source: Aquastat, IFPRI, IMF, ourworldindata.org

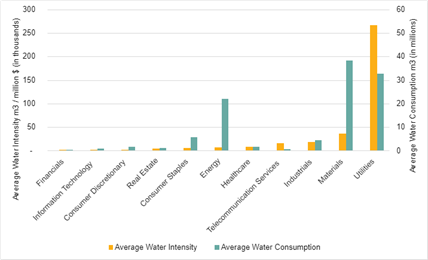

Putting Water Metrics into Practice: Water Use by Sector

Unavoidably, increasing stress will affect people and companies located in those countries. We highlight this trend and discuss ways to manage its effects. One avenue is to provide tools and metrics to better monitor water consumption and withdrawal.

As these metrics become available, investors could make more informed decisions and increase the impact on their financial eco-systems. For instance, investors may decide to divest from or engage companies that misuse water resources.

Water-related risks have material financial impacts. For example, if the company faces increased water input costs, production could become uneconomical. Moreover, heavy water-consuming companies are often perceived as taking advantage of the resource and causing economic harm to society. Hence, companies with high water consumption and water intensity have potentially high exposure to water risk.

In Exhibit 2, water intensity and water consumption (in total cubic meters) of sectors are presented. The Utilities sector takes a clear first place for water intensity as water is necessary for many electricity-generating activities, with the Materials and Industrials sectors in second and third, respectively. For water consumption, the Materials sector is the top consumer, driven by high water demanding steel producers and mining companies, with Utilities in second and Energy in third, respectively.

Exhibit 2: Water Use by Sector

Source: Morningstar, Sustainalytics

Water Intensity and Firm Characteristics

Looking at a global sample of 4,914 firms from 2020, our analysis shows that firms with high water intensity display high ESG risk, high return, high standard deviation of returns, and high downside deviation of returns (see Exhibit 3). Water intensity, however, weakly relates to risk-adjusted return.

Exhibit 3: Correlations Between Firm Water Intensity and Firm Characteristics

Source: Morningstar, Sustainalytics

Sustainalytics Water Metrics

While building investment strategies, savvy investors look at water risk issues using a holistic approach by considering company and regional factors. At the company level, it is crucial to pay attention to such metrics level of water consumption, water withdrawal, and water intensity. Second, it is important to review the corporate policies and programs to reduce the company's risk exposure, which reflects the company's preparedness to manage these risks. Investors should also assess the business's location to determine if the country or region in which the company operates is exposed to other water risks.

These indicators are measured through Sustainalytics' comprehensive ESG Risk Ratings methodology. Our findings within this framework suggest that reducing exposure to water stress correlates to ESG risk exposure. Investors can use this tool to integrate relevant data into their analyses to reduce portfolio exposure to water-related risks.

The Emergence of Water Risk: From Marginal to Systemic

Our study shows that water stress has implications beyond the immediate use of water, as water stress affects all the aspects of the economy and well-being of society. Therefore, monitoring water usage indicators at the country and firm levels is urgently necessary for country policymakers, company executives, and shareholders alike.

You can access the full report, Water-Related Risks and Challenges: A Quantitative Research Perspective, for additional insight.

Sources:

1. Fishman, C. (2011, 00:22:14); “The Big Thirst: The Secret Life and Turbulent Future of Water”; audible, accessed (06.15.2020) at: https://www.audible.ca/pd/The-Big-Thirst-Audiobook/

[ii] The forecast for withdrawal growth is inspired by 2030 Water Resource Groups exhibit 4, titled Aggregated global gap between existing accessible, reliable supply and 2030 water withdrawals, assuming no efficiency gains. Due to not having basin level data, we subbed in Aquastat sector data as of 2017 as our base information. Note that the model also differs in that it uses total renewable water resources, and not relevant supply quantity. The following inputs are as follows. 2002 to 2017 and water withdrawals for Industrial, Municipal and Agricultural, based on Aquastat data. 2002 to 2017 desalinated water produced, direct use of treated municipal wastewater, direct use of agricultural drainage water based on Aquastat data, with 2030 forecasted created based on the growth trajectory from 2012 to 2017 at the country level. Agriculture growth based on 2030 agricultural production forecast for 2030 from IFPRI, IMPACT Model v 3.3. Industrial growth based on IMF country GDP forecasts and actuals, 2018 to 2026. Municipal growth based on Population growth for countries using 2018 to 2030 actuals and estimates from ourworldindata.org. Agricultural and industrial efficiency improvements from www.2030wrg.org. Municipal efficiency improvements from 2002 to 2017 differential in Aquastat Municipal withdrawals and population growth at the global level. 2017 SDG 6.4.2. Water Stress (%) from Aquastat. Total renewable water resources, environmental flow requirements for 2030 from Aquastat.

2030 Water Resources Group (2009); “Charting Our Water Future”; 2030 Water Resources Group ; accessed (04.05.2021) at: https://www.2030wrg.org/wp-content/uploads/2012/06/Charting_Our_Water_Future_Final.pdf

[© FAO] (2021); AQUASTAT Database; accessed (28.04.2021 18:25) at: http://www.fao.org/aquastat/statistics/query/index.html?lang=en

Our World in Data (2021); The Population Growth Rate by Country Database; accessed (28.04.2021) at: https://ourworldindata.org/future-population-growth

International Food Policy Research Institute (2019); Source: IFPRI, IMPACT Model version 3.3, Latest update as of January 2019; accessed (28.04.2021) at: https://www.ifpri.org/publication/impact-projections-food-production-consumption-and-hunger-2050-and-without-climate-0

International Monetary Fund (2021); Real GDP Growth; Database; accessed (28.04.2021) at: https://www.imf.org/external/datamapper/NGDP_RPCH@WEO/OEMDC/ADVEC/WEOWORLD