As growing pressure to cut GHG emissions is causing Western oil majors to sell their high-carbon assets, it is expected that National Oil Companies (NOCs) will pick up some of the production.1 For investors holding an interest in or considering investing in NOCs or sovereign debt, it is worth assessing how fossil fuel production shifts will impact their portfolio’s alignment with climate ambitions and ESG values.

Current State of NOCs and Oil Majors

International oil majors, such as Exxon, Equinor, Chevron, BP plc, Shell, TotalEnergies, ConocoPhillips, and Eni SpA, face pressure from a growing number of shareholders and investors to transition away from high-carbon product portfolios. In response, there is a trend in the last few years of US and Europe oil majors selling off portions of their higher carbon assets (e.g., Canadian Oil Sands), leaving purchase opportunities for other oil and gas players.

In comparison, National Oil Companies (NOCs), which are majority or wholly owned by the government, face domestic political pressures often to continue expenditure on new oil and gas projects particularly given that some states, such as Russia and Saudi Arabia, have economies tied to fossil fuels. Consequently, some NOCs are incentivized to purchase the high carbon assets that oil majors no longer want.

Approximately half of today’s worldwide oil supply is provided by NOCs,1 and with the potential for the state-owned companies to purchase more fossil fuel assets, this share may increase in the following years. This situation raises the question - what are the ESG risks associated with NOCs owning a larger portion of fossil fuel assets?

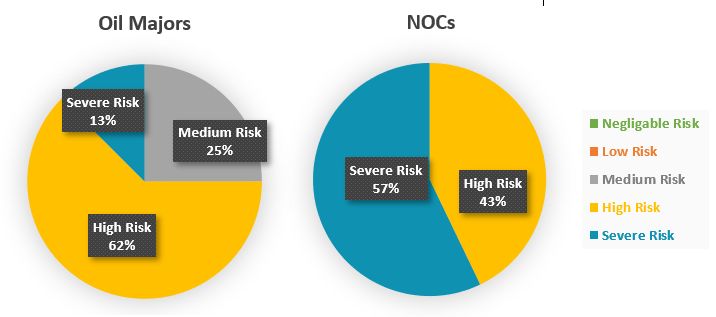

Overall ESG Performance

Using Sustainalytics’ ESG Risk Ratings, which assesses company’s exposure to industry specific material ESG issues (MEIs) and how well a company is managing those risks, we compared the average scores of oil majors to NOCs for a sample set of companies. The majority of oil majors have high-risk scores (30-40), compared to NOCs with severe risk scores (40+) (Figure 1).

Figure 1: ESG Risk Rating Scores (Average)

Source: Sustainalytics

Exposure to ESG Risk

In terms of exposure to MEIs, on average NOCs and oil majors have similar scores, including under Human Capital, Resource Use, Business Ethics, and Emissions, Effluent and Waste MEIs (Figure 2). However, NOCs generally have higher exposure to Bribery and Corruption issues (Figure 2), given that their operations are often located in regions where corruption incidents are more prevalent.

Figure 2: MEI Exposure Score (Average) of Oil Majors versus NOCs

-of-oil-majors-versus-nocs.png?Status=Master&sfvrsn=5ba53499_1)

Source: Sustainalytics

Management of ESG Risks

On the management side, there is a greater difference in how the two types of companies score, with NOCs generally having a weaker management score under the MEIs. As seen in Figure 3, the average Corporate Governance management score for NOCs (48-Average) is significantly lower (13 points) compared to oil majors (61-Strong). Weaker governance structures, practices, and behaviours can affect a company’s ability to manage MEIs and execute its ESG strategy. NOCs also score notably lower under Community Relations, Bribery and Corruption, Carbon – Own Operations, Land Use and Biodiversity, and Resource Use (figure 3), signalling that these companies have gaps in their policies, programs, management systems and/ or have poor track records associated with managing these MEIs.

Figure 3: MEI Management Score (Average) of Oil Majors versus NOCs

-of-oil-majors-versus-nocs.png?Status=Master&sfvrsn=da5fde9e_1)

Source: Sustainalytics

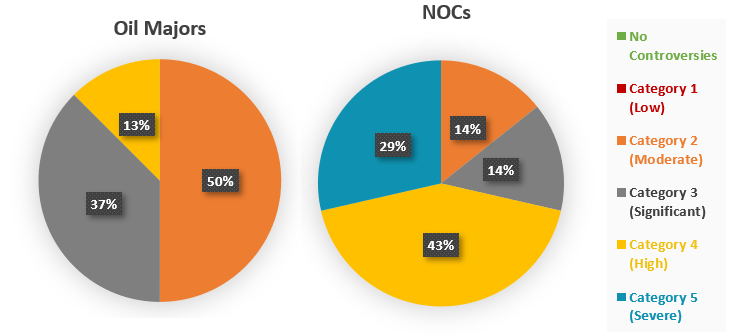

Involvement in Controversies

In addition to assessing companies’ ESG Risk Rating, we overlaid Sustainalytics’ Controversies Research - which identifies companies involved in controversies that may negatively impact stakeholders, the environment, or the company’s operations, and rates them on a scale from 1 to 5 (5 being the highest risk). We found that NOCs face more Category 4 and 5 controversies compared to oil majors (Figure 4).

Figure 4: Highest Controversy Level (Average) of Oil Majors versus NOCs

Source: Sustainalytics

Looking Forward

Global oil demand is set to continue rising,2 meaning that it is likely that high carbon assets will continue being acquired by weaker ESG performers, including some NOCs.

There has been some positive momentum on the issue, for instance, at COP 26, Saudi Arabia, and India, two countries with large NOCs, pledged to reach net-zero GHG emissions in the next decades.3 In addition, in 2021, the Assessing Sovereign Climate-related Opportunities and Risk (ASCOR) framework was launched to assist investors in assessing sovereign climate-related risks and opportunities.4

For investors considering investing in NOCs or sovereign debt, a strong understanding of the ESG risks NOCs face is critical to assess alignment with ESG values and risk appetite. Learn more about how Sustainalytics’ ESG Risk Ratings and Controversy Research can support investors with complex considerations in their portfolio selection.

Sources:

[1] IEA (2020), The Oil and Gas Industry in Energy Transitions. https://www.iea.org/reports/the-oil-and-gas-industry-in-energy-transitions

[2] IEA (2022), Oil Market Report - February 2022. Accessed at: https://www.iea.org/reports/oil-market-report-february-2022

[3] NPR (2021), Saudi Arabia pledges net-zero greenhouse gas emissions by 2060. https://www.npr.org/2021/10/23/1048655294/saudi-arabia-zero-emissions-climate-change-2060; BBC (2021), COP26: India PM Narendra Modi pledges net zero by 2070. https://www.bbc.com/news/world-asia-india-59125143

[4] UNPRI (2021), The ASCOR Project: Assessing Sovereign Climate-related Opportunities and Risks. https://www.unpri.org/news-and-events/the-ascor-project-assessing-sovereign-climate-related-opportunities-and-risks/7681.article