Strategy for Financing the Transition to a Sustainable Economy

On July 6th, the European Commission published its Strategy for Financing the Transition to a Sustainable Economy, the successor of the EU’s Sustainable Finance Action Plan, which launched in 2018. The strategy focuses on transforming the financial system and financing transition plans, building on the 2018 Action Plan, which centered on developing the EU Taxonomy, putting in place disclosure regimes, and developing tools for the market to develop sustainable investment solutions and prevent greenwashing.

The new strategy identifies four main areas for action for the financial system to fully support the transition to a sustainable economy:

- Financing the transition: tools and policies to finance transition plans and reach climate and other environmental goals

- Inclusiveness: access to sustainable finance for individuals and small and medium companies

- Financial sector resilience and contribution: support the financial sector to contribute to meeting the EU’s Green Deal targets, becoming resilient, and combat greenwashing

- Global ambition: collaborating globally and promote an ambitious global sustainable finance agenda

The EU Taxonomy remains a key building block of the EU’s sustainable finance plans, and much further development is laid out in the strategy:

- Including the business activities that proved too politically challenging to include in last April’s Climate Delegated Act (e.g., agriculture and certain energy sectors such as nuclear and gas) in a complementary Delegated Act. In other words, the criteria for how such activities can be considered sustainable are being developed. Adoption of the act is expected after this summer.

- The criteria for the remaining Taxonomy objectives, water, circular economy, pollution prevention and biodiversity, will be adopted in the first half of 2022 and apply from 2023.

- A report on a social taxonomy is expected by the end of 2021.

- Work on a transition taxonomy and a taxonomy recognizing economic activities that perform at an ‘intermediary level’ will continue.

Taxonomy Rules on Reporting by Companies and Financial Institutions are now Available

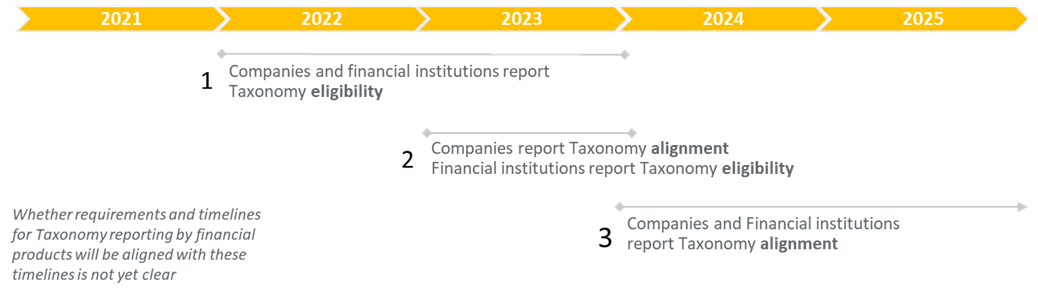

Together with the new strategy, the Commission also published the rules for how and when companies (‘non-financial undertakings’) and financial institutions (‘financial undertakings’) need to do their Taxonomy-related reporting, the Delegated Act for Taxonomy Regulation article 8. A key change compared to previous versions and recommendations is that the timelines have been pushed out. The timing mismatch between when companies start reporting, and financial undertakings need to start using companies’ reported data has thereby been largely resolved. Both financial and non-financial undertakings start reporting on only a small subset of the requirements in 2022 (‘eligibility’ data mainly). As we described in a recent blog article, this data won’t be very meaningful and may in fact be misleading. However, the EU clearly favored this approach versus redoing the political process of drafting and approving new regulations to amend the timelines in the Taxonomy Regulation.

Effective in 2023, companies need to start reporting their own Taxonomy alignment, and the latest rules lay down the KPIs, content and presentation in detail. Financial undertakings only need to start reporting their Taxonomy alignment beginning in 2024, at which time the necessary 2023 reported data by the non-financial undertakings they hold in their portfolios and on their books is available. Essentially, this is a two-year delay in the implementation of the regulation. Critically, what is still unclear, is how this relates to the timelines of when financial products that fall under the regulation need to report their Taxonomy alignment. This is covered in a different set of rules combined with the Sustainable Finance Disclosure Regulation rules on what financial products need to report. We assume these timelines will be harmonized with the timelines for financial undertakings; however, this is still unclear.

Figure 1: Summary timeline of Taxonomy implementation, Source: Sustainalytics

Besides the timelines, several other elements are worth noting:

- It seems that the final rules do not allow for the use of estimates of Taxonomy alignment. It appears that Do No Significant Harm principal estimations are permitted, but only on non-EU companies that report on the Substantial Contribution and the Minimum Safeguards criteria of the Taxonomy themselves. Also, the estimated data needs to be reported separately from the key performance indicators on companies in the scope of the regulation; This could block financial undertakings from estimating Taxonomy alignment. The draft act published in May had fully ruled out estimates, and it also excluded non-EU companies entirely from what financial undertakings could report on. This triggered pushback from various sides because of the negative consequences, as we described in our previous blog article and advised against in Morningstar's letter in response to the consultation on the draft rules. While it seems a positive development that estimates are no longer fully banned, it is very much a question in how many cases this approach can actually be used and whether this makes any material difference for global investors. Interestingly, estimates are not allowed at all on European companies that are not required to report their alignment (i.e., EU small and mid-caps), supposedly incentivizing those companies to consider voluntarily reporting Taxonomy data.

- However, alignment data reported voluntarily, for instance, by EU small caps or non-EU companies, cannot only be included in the KPIs of financial undertakings until 2025. Presumably, the EU wants to avoid investors putting too much pressure on smaller companies to report alignment data and prefers first to figure out the exact requirements for those companies and how to support them in doing so.

- Derivatives and sovereign assets are fully out of scope, at least until the next review of the regulation.

After close to a year where we saw our clients primarily focus on the Sustainable Finance Disclosure Regulation, we now see a shift back to the Taxonomy given its tight timelines and complexities. Investors are looking ahead and figuring out what they need to comply with the regulation and how they can use the Taxonomy as a broader framework for investment decision-making and impact reporting.

Sustainalytics recently launched a comprehensive new EU Taxonomy Solution that aims to support investors through the process. Get in touch to learn more.