India saw several enhancements to its corporate governance framework on April 1, 2019, when the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2018 came into effect. The amendments to SEBI listing regulations reflect the adoption of a slew of recommendations made by the “Kotak Committee” – a blue-ribbon panel formed in June 2017 under the chairmanship of banker Uday Kotak, with the purpose of improving corporate governance standards in India. The committee’s recommendations are being phased in between October 1, 2018 and April 1, 2020.

The amendments occur against a backdrop of several widely publicized corporate governance controversies, including the ICICI Bank-Videocon scandal that led to the downfall of celebrated CEO Chanda Kochhar, the unanticipated Infrastructure Leasing & Financial Services’ defaults, the abrupt mid-term resignation of dozens of auditors of publicly-listed Indian companies, and Yes Bank’s governance crisis.

In this blog post, we examine the most salient of the changes that entered into force on April 1.

Board structure

The new regulations now explicitly prohibit members of “the promoter group[i] of the listed entity” and interlocked directors from serving as independent directors[ii]. This stricter definition can be expected to exacerbate India’s already low rate of board independence: as of December 31, 2018, 37% of the S&P BSE SENSEX[iii] company boards lacked an independent majority, whilst 53% of boards included more than two company executives. Notably, the Kotak Committee had proposed SEBI Listing Regulations be amended so that all listed entities’ boards are at least 50% independent, but the recommendation was not implemented. Per the Companies Act, only listed entities having an executive chairman/chairman related to the promoter are required to have the board at least half independent, otherwise the required board independence level is one-third.

Board diversity

While India has long drawn criticism for its lack of board diversity, the new regulations require that at least one independent female director is appointed to the boards of the top 500 listed entities[iv] by April 1, 2019, and on the boards of the top 1000 listed entities by April 1, 2020. As of December 31, 2018, 10% of the S&P BSE SENSEX companies featured no independent female directors on the board.[v] However, we highlight that current practice in developed markets is that women constitute 20% or more of the board’s membership.

Overboarding

In a bid to mitigate overboarding concerns, the new regulations cap a director’s maximum number of directorships on the boards of listed companies to eight[vi] by April 1, 2019, and to seven by April 1, 2020. In addition, the amendment stipulates a director serving as a managing director/full time director in a listed company can “serve as an independent director in not more than three listed entities”. As of December 31, 2018, 60% of the S&P BSE SENSEX companies featured at least one director serving on the board of five or more listed entities.

Other board regulations

The new regulations also aim to encourage board refreshment by stating that no director is eligible to continue serving or to be appointed as director after having reached the age of 75, unless a special resolution[vii] on the matter is adopted.[viii] Notably, HDFC Bank Chairman Deepak Parekh narrowly avoided defeat on his reelection vote at the 2018 AGM, when nearly 23% of the votes dissented on the extension of his term beyond October 2019, when he will attain the age of 75. The reappointment of several other prominent figures such as Shree Cement Chairman B. G. Banguras will soon be put to the same test.

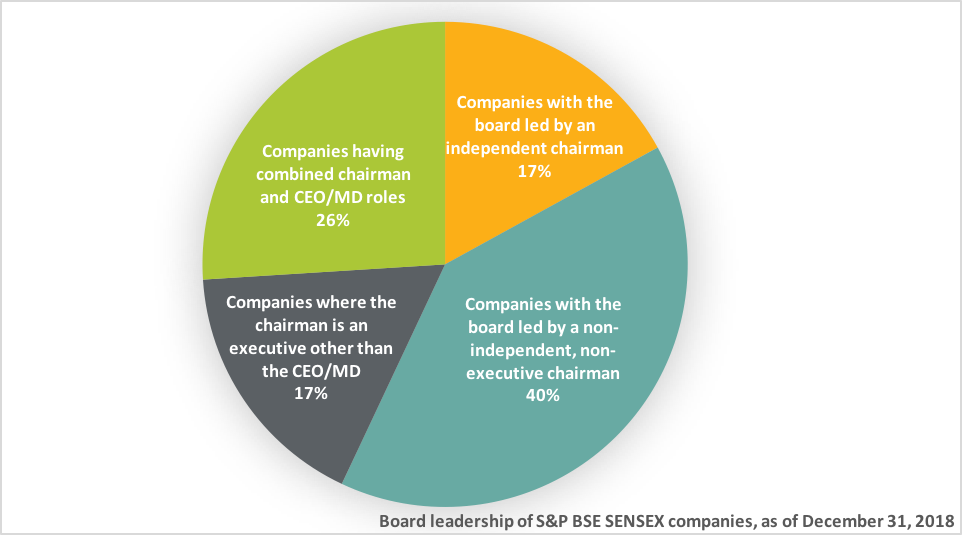

Perhaps the most substantial change introduced by the Amendment is that by April 1, 2020, the top 500 listed entities are required to appoint a non-executive chairman not related to the managing director or CEO as per the Companies Act, 2013[ix]. As of December 31, 2018, 43% of S&P BSE SENSEX boards were chaired by an executive director, whilst only 17% were led by an independent director.

Audit-related issues

The new regulations aim to create more transparency on auditor resignations by requiring that listed companies disclose “detailed reasons” within 24 hours of receiving a resignation from the auditor.

As previously noted, 2018 was marked by the abrupt mid-term resignation of dozens of auditors of Indian listed companies. Manpasand Beverages Ltd shares fell by 20% in one trading day after auditors Deloitte Haskins & Sell announced their departure. The resignation of Price Waterhouse & Co Chartered Accountants LLP as Vakrangee Ltd’s auditors sent shares diving by almost 80% in the following months. In both instances, the auditors quit over lack of adequate information, just days before finalizing the annual accounts. Subsequently, the Ministry of Corporate Affairs opened a probe into the auditor exodus, linked by many to the ban imposed by SEBI on PWC network firms in early 2018[x].

Related party transactions

The new regulations expand the definition of related parties to include “any person or entity belonging to the promoter or promoter group of the listed entity and holding 20% or more of shareholding in the listed entity”, whilst also requiring the disclosure of transactions “with any person or entity belonging to the promoter/promoter group which hold(s) 10% or more shareholding in the listed entity”. Previously, certain promoter/promoter group entities did not qualify as related parties per the definitions set forth in the Companies Act, 2013 and applicable accounting standards[xi], so their transactions with the company were not treated as related party transactions under SEBI Listing Regulations. Related party transactions have been top-of-mind with Indian corporate governance ever since the Satyam fraud in 2009 and have more recently been brought to the fore as a result of the ICICI Bank-Videocon scandal.

The coming year will likely witness significant efforts from Indian companies in achieving compliance with the more stringent corporate governance requirements underway. Nevertheless, it remains to be seen how the ongoing reform will manage to address the greatest challenge faced by the country in improving its corporate governance: the agency problem between promoters and minority shareholders.

Endnotes

[i] In general terms, promoters are persons or groups exercising control over a company. In this context, the notion of control is separated from cash flow rights, as promoters typically achieve control through cross-shareholdings and pyramidal ownership structures. The term was first defined in the Companies Act, 2013 under section 2(69), and has since been defined in several other regulations, more recently in the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018. Notably, in India all listed companies are required to provide a detailed disclosure of their ownership structure on a quarterly basis, which distinguishes between two major categories of owners: promoters, and non-promoters.

[ii] Namely, the definition has been expanded to exclude any director “who is not a non-independent director of another company on the board of which any non-independent director of the listed entity is an independent director”.

[iii] The S&P BSE SENSEX is the bellwether index for Indian stocks.

[iv] The ranking is determined on the basis of market capitalization.

[v] Per current regulations, companies are required to appoint one female director on the board, regardless of independence.

[vi] As of December 31, 2018, none of the S&P BSE SENSEX companies featured a director serving on more than eight listed entities on their board.

[vii] Special resolutions are resolutions requiring the approval of 75% of the votes cast in order to be passed.

[viii] The Companies Act provides that a managing director, whole-time director, or manager cannot be appointed after reaching the age of 70 unless a special resolution is passed on the matter.

[ix] Listed entities having no “identifiable promoters as per the shareholding pattern” are exempt from the requirement.

[x] In January 2019, SEBI barred the PWC network firms from auditing listed companies in India for a two-year period, on the grounds that the auditing firms failed to detect the Satyam scam which was revealed in 2009.

[xi] As concluded in the Kotak committee’s report.