As mandatory climate-related reporting continues to advance around the world, companies headquartered in the United States and Canada are subject to pending disclosure rules from securities regulators. This article focuses on the proposed scope 3 emissions disclosure rules in North America, providing insights into companies’ levels of preparedness to respond, and the challenges and solutions being discussed through engagement strategies with high or severe risk companies in the Morningstar Sustainalytics Ratings universe.1

Examining the SEC and CSA Proposals for Scope 3 Emissions Disclosure

In recent years, both the Securities and Exchange Commission (SEC) in the U.S. and the Canadian Securities Administrators (CSA) have proposed rules to enhance corporate climate disclosures. Of particular interest are the provisions related to scope 3 emissions.

Compared to scope 1 and 2 emissions, which refer to the direct emissions from owned or controlled sources and indirect emissions from the generation of purchased energy respectively, scope 3 emissions are all other indirect emissions that derive from an organization’s value chain. It is critically important for companies to account for their scope 3 emissions as they are estimated to take up more than 70% of a business’ total carbon emissions on average.2 The share of scope 3 emissions can be as high as 99.84% in financial services and 80.85% for oil and gas.3

Under the SEC proposal, issuers would be required to disclose their scope 3 emissions if they are material or if the issuer has set targets for them.4 In Canada, the CSA is considering mandating a comply-or-explain approach to all three emission scopes or to scope 2 and 3 emissions only.5

While the comment period for both proposals has ended, the regulatory agencies have yet to finalize the rules. The CSA announced in October 2022 that it was considering the international consensus on the topic.6 Meanwhile in the U.S., there are indications that the SEC may delay launching the rules until fall 2023.7 Legal challenges against the rules are also expected once they are finalized, which could complicate adoption.

Challenges With Scope 3 Emissions Reporting

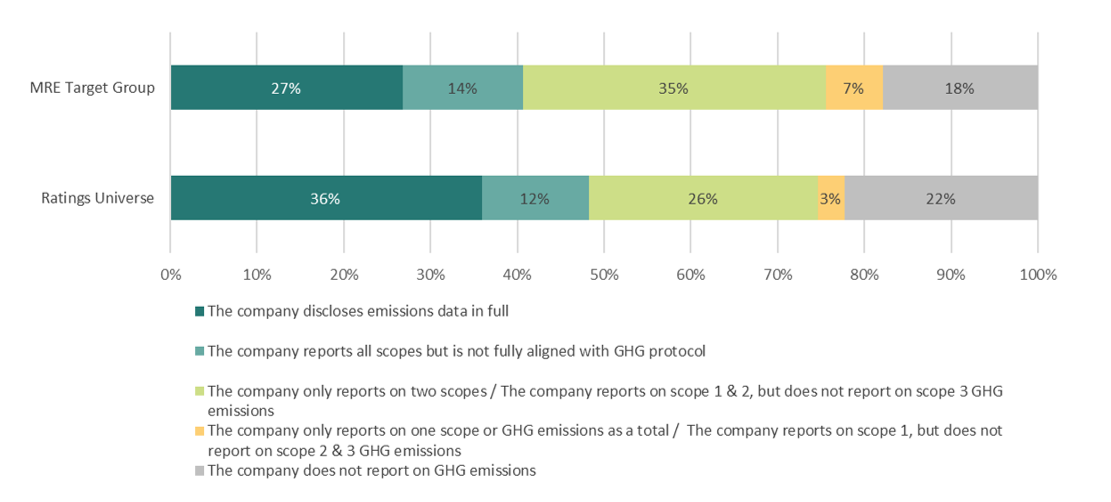

In anticipation of the finalized rules, North American companies are struggling to understand, calculate and disclose their scope 3 emissions. Only 36% of the companies included in Sustainalytics’ Ratings universe disclose all three types of emissions in line with the Greenhouse Gas (GHG) Protocol (see Figure 1 below).

Of the companies targeted by Sustainalytics Material Risk Engagement — those companies assessed as having high or severe risk based on Sustainalytics ESG Risk Ratings — only 27% disclosed all three emission scopes. Overall, more than half of the companies in both groups are either not disclosing GHG emissions at all or have only reported on one or two scopes.

Figure1. Scope of GHG Reporting for Issuers Headquartered in the U.S. and Canada

Source: Morningstar Sustainalytics. The data for this analysis was retrieved on June 1, 2023, from Sustainalytics' Ratings Universe. For informational purposes only.

The GHG Protocol Corporate Standard divides scope 3 emissions into upstream and downstream emissions and then classifies them into 15 distinct categories.8 So, to achieve full disclosure of emissions data, a company’s scope 3 emissions inventory should be disclosed by category. But for many companies, this is no easy task.

Common challenges with scope 3 reporting are often discussed during conversations with companies through Sustainalytics’ Material Risk Engagement program. These companies regularly cite issues with data quality and calculations; lack of accounting or estimation methodologies; and conglomerate, decentralized or geographically diverse organizational structures that hinder data collection and assimilation. However, even without mandatory reporting rules from the SEC and CSA, the need for consistent, comparable scope 3 emissions data will continue to increase, irrespective of the challenges companies are facing.

Why Companies Should Act Now to Improve Their Scope 3 Disclosures

Although it may take some time before the scope 3 emissions disclosure rules take effect in North America, companies can benefit from understanding and gradually working towards reporting their scope 3 emissions now. Such an exercise can offer deeper insight into a business’ carbon footprint across its value chain and identify decarbonization opportunities.

Other developments within different jurisdictions and standard setting organizations are also driving companies towards enhanced transparency. For example, the U.S. federal government proposed in 2022 that major federal contractors (US$50 million in annual contract obligation) must report on their scope 3 emissions; California and New York introduced bills similar to the SEC’s proposal; scope 3 disclosures will be required under the European Union’s Corporate Sustainability Reporting Directive, which comes into force January 2024 and will likely impact more than 3,000 U.S. and 1,300 Canadian companies.9 The International Sustainability Standards Board has also issued its inaugural climate-related disclosure standard that includes scope 3 emissions in June 2023. Companies need to be prepared for the ever-growing demand for emissions data.

Investor Engagement Strategies to Improve Corporate Scope 3 Disclosure

Engagement can help investors assess a company’s preparedness for the proposed disclosure rules, understand challenges they are facing, and help to implement solutions. By first discussing the potential benefits of enhanced transparency around scope 3 emissions, investors can then inspire companies to take steps to improve disclosure.

Companies wrestling with data quality and calculation uncertainty can be directed to the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard and its supplemental document, Technical Guidance for Calculating Scope 3 Emissions. These documents provide guidance on calculation methods, data sources, and examples of calculating scope 3 emissions as well as several cross-sector and sector-specific calculation tools.

But understanding scope 3 emissions standards isn’t necessarily enough. A company often needs to invest in resources dedicated to performing the calculations and managing the emissions inventory once it is established. Carbon accounting software can help with automated data processes, measurement conversions, calculations, and forecasts. These systems will also come in handy for internal audit and external verification.

In the absence of data, estimation is an accepted first step in the development of a scope 3 emissions inventory. According to the GHG Protocol, a company needing to collect a large quantity of data for a particular scope 3 category may find it impractical or impossible to collect the data from each activity in the category. In such cases, companies may use appropriate sampling techniques to extrapolate data from a representative sample of activities within the category.10

In addition, some sectors are developing their own scope 3 estimation methodologies based on guidance from the GHG Protocol. As an example, oil and gas companies can look to the International Petroleum Industry Environmental Conservation Association for methodologies to inform scope 3 GHG emissions estimation and approaches. Financial institutions endeavoring to disclose against their financed emissions (scope 3, category 15) can refer to the Global GHG Accounting and Reporting Standard by the Partnership for Carbon Accounting Financials.11, 12 Whichever way an estimate is calculated, the company should disclose the methodology used.

Performing and disclosing these calculations can also be done in phases. A company can be encouraged to focus efforts on its most material scope 3 category first and disclose the reasons why it is not reporting against the remaining categories. Finally, market leaders should be expected to demonstrate support and guidance with their suppliers’ capacity to calculate carbon emissions, which in turn could enable multiple companies to move from estimated to actual scope 3 data.

Developing a scope 3 emissions inventory is complex and built on cumbersome processes that many North American companies are struggling with. Even though the task can be daunting, solutions are available and flexibility in disclosure remains on the table, for now. There are obvious environmental and financial benefits to understanding and reporting value chain emissions. Investors and market leading companies should continue to encourage voluntary corporate transparency with a solutions mindset, so that companies are prepared to respond to evolving global market requirements and more importantly, truly understand and address the impact of their carbon footprint.

To learn more about opportunities to engage with companies on their GHG emissions and disclosures, visit our Engagement Services web page or contact us.

References

- The Morningstar Sustainalytics Ratings universe comprises approximately 5,000 large and medium market cap investable issuers in developed and emerging markets.

- Global Compact Network UK. n.d. “Scope 3 Emissions.” https://www.unglobalcompact.org.uk/scope-3-emissions/.

- CDP. n.d. “CDP Technical Note: Relevance of Scope 3 Categories by Sector.” https://cdn.cdp.net/cdp-production/cms/guidance_docs/pdfs/000/003/504/original/CDP-technical-note-scope-3-relevance-by-sector.pdf.

- Securities and Exchange Commission. 2022. “The Enhancement and Standardization of Climate-Related Disclosures for Investors.” https://www.federalregister.gov/documents/2022/04/11/2022-06342/the-enhancement-and-standardization-of-climate-related-disclosures-for-investors#h-20.

- Keyes, S. and Lanz, D. 2022. “A Comparative Analysis of U.S. (SEC) and Canadian (CSA) Climate Disclosure Proposals.” ESG Global Advisors. https://www.esgglobaladvisors.com/news-views/a-comparative-analysis-of-u-s-sec-and-canadian-csa-climate-disclosure-proposals/.

- Canadian Securities Administrators. 2022. “Canadian securities regulators consider impact of international developments on proposed climate-related disclosure rule”. Official CSA press release, October 12, 2022 https://www.securities-administrators.ca/news/canadian-securities-regulators-consider-impact-of-international-developments-on-proposed-climate-related-disclosure-rule/.

- Rives, K. 2023. “SEC climate disclosure rule delayed until fall, former commissioner says.” S&P Global Market Intelligence, April 28, 2023. https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/sec-climate-disclosure-rule-delayed-until-fall-former-commissioner-says-75479173.

- Greenhouse Gas Protocol. 2011. “Corporate Value Chain (Scope 3) Accounting and Reporting Standard.” https://ghgprotocol.org/sites/default/files/standards/Corporate-Value-Chain-Accounting-Reporing-Standard_041613_2.pdf.

- Worland, J. 2023. “Why U.S. Companies Should Pay Attention to Europe’s New Climate Rules.” Time, May 25, 2023. https://time.com/6282880/why-eu-climate-corporate-disclosure-rules-matter/.

- Greenhouse Gas Protocol. 2022. “Technical Guidance for Calculating Scope 3 Emissions, Appendix A: Sampling”. https://ghgprotocol.org/sites/default/files/2022-12/AppendixA.pdf.

- International Petroleum Industry Environmental Conservation Association. 2016. “Estimating petroleum industry value chain (Scope 3) greenhouse gas emissions. Overview of methodologies.” https://www.ipieca.org/resources/estimating-petroleum-industry-value-chain-scope-3-greenhouse-gas-emissions-overview-of-methodologies.

- Partnership for Carbon Accounting Financials. 2022. “The Global GHG Accounting and Reporting Standard Part A: Financed Emissions. Second Edition.” https://carbonaccountingfinancials.com/files/downloads/PCAF-Global-GHG-Standard.pdf.