Key Insights:

- Reported capital investments reached USD 500 billion, but average taxonomy-alignment levels have not increased.

- Average alignment levels reported this year are quasi-unchanged compared to last year’s alignment levels.

- Non-financial companies reporting above-zero data have 28% of their capital investments (capex) aligned with the taxonomy, on average.

- Alignment levels are expected to increase from next year, when alignment reporting on the four new environmental objectives of the taxonomy becomes mandatory. Currently, reporting on these objectives is limited.

- It is still early days for taxonomy reporting and investors should be mindful of reported data inaccuracies, incompleteness, and misalignment.

The EU Taxonomy is a classification system that was introduced in 2020 to help companies and investors identify environmentally sustainable economic activities to make sustainable investment decisions, with the ultimate goal of making Europe the world’s first climate-neutral continent by 2050.

The EU Taxonomy is integrated into EU regulatory frameworks to promote sustainable finance and corporate transparency, including the Sustainable Finance Disclosure Regulation (SFDR) and MiFID II sustainability preferences, under which Article 8 and Article 9 funds must provide taxonomy-alignment data. The EU Taxonomy is also increasingly used by various actors to define and assess business strategies, transition planning, investing and lending.

Last year, large, listed companies based in the EU started reporting on their taxonomy-aligned activities against the two climate objectives – climate change mitigation and climate change adaptation. This year, companies must also report on alignment against the taxonomy’s other four environmental objectives: circular economy, pollution prevention, biodiversity protection, and water and marine resources.

In our first EU Taxonomy Reporting Review, we examined alignment key performance indicators (KPIs) on revenue, opex, and capex on more than 1,300 non-financial companies over the last two reporting years, to understand the progress companies are making in reporting their taxonomy alignment and commitment to the investments needed in the transition to a more sustainable economy.

Average Taxonomy-Alignment Levels Are Quasi-Unchanged

We found that over the last year, average taxonomy-alignment levels have remained quasi-unchanged. The average aligned revenue increased modestly from 12.2% for 2022 to 12.9% for 2023, while the average aligned opex slightly decreased from 14.6% to 14.3%. Finally, the average capex alignment exhibited a marginal increase from 17.9% to 18.6%.

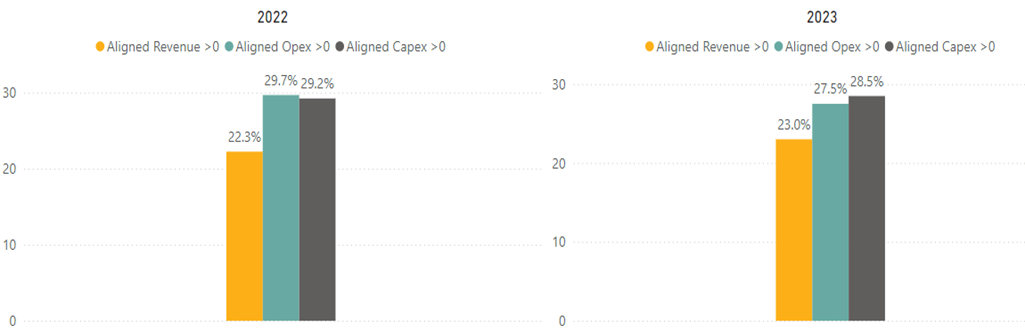

Because 42% of the covered companies reported zero alignment, we also calculated above-zero taxonomy alignment for 2023 (Figure 1 below). And we found that companies reported an average of 23% aligned revenue, 27.5% aligned opex, and 28.5% aligned capex. These alignment levels are also very similar to those observed for 2022. Here, like above, capex presents the highest alignment percentage among the three taxonomy KPIs.

Figure 1. Above-Zero Average Alignment of Revenue, Opex and Capex

Source: Morningstar Sustainalytics. For informational purposes only.

Alignment levels are expected to increase next year, when alignment reporting on the four new environmental objectives of the taxonomy (i.e., circular economy, pollution prevention, biodiversity protection, and water and marine resources) becomes mandatory.

Utilities Companies Have the Highest Alignment Numbers

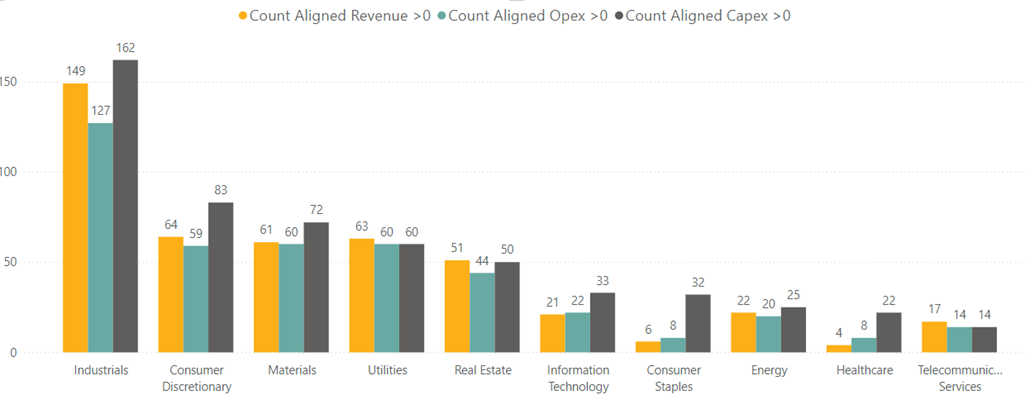

Looking across the sectors, we see that industrials companies represent the largest portion (30%) of our sample of 2023 reporting companies, followed by consumer discretionary (15%) and materials (13%). These numbers somewhat reflect the make-up of the EU economy. The lowest reporting sectors are telecoms, healthcare and energy.

Figure 2. Number of Companies Reporting Above-Zero Taxonomy Alignment Per Sector

Source: Morningstar Sustainalytics. For informational purposes only.

Note: Data covers FY2023.

However, when it comes to taxonomy-alignment, utilities stands out as the sector with the highest numbers across all three KPIs. Utilities companies report an impressive 77% average capex alignment, while their average revenues are 45% aligned. This sector is pivotal in driving the energy transition towards low-carbon technologies. Meanwhile, other high-emitting sectors, such as materials and energy, exhibit low alignment figures, with only 18% of capex in these sectors aligned with EU sustainable objectives.

Figure 3. Taxonomy-Alignment Above-Zero Per Sector

Source: Morningstar Sustainalytics. For informational purposes only.

Note: Data covers FY2023.

In terms of capex investments since companies first started reporting, the utilities sector also leads, with approximately USD 240 billion, accounting for more than 50% of the total reported aligned investments. The consumer discretionary sector follows, with capex investments of USD 104 billion. The primary driver behind the latter is the capital-intensive automotive industry, which includes large-scale investments related to the transition to electric vehicles, battery production, and the development of alternative fuels. Industrials, meanwhile, is trailing with USD 78 billion, contributing almost 17% of the total.

In total, aligned capital investments reported for 2022 and 2023 and for which we have collected data, amount to about USD 500 billion.

In line with this sector breakdown, we list below the six activities that benefit the most from the investments. Featured at the top are electricity and transport-related activities.

Figure 4. Aligned Investments for Top Activities

Source: Morningstar Sustainalytics. For informational purposes only.

Note: Based on FY2022 and FY2023 capex data.

Climate Change Mitigation Remains the Dominant Environmental Objective

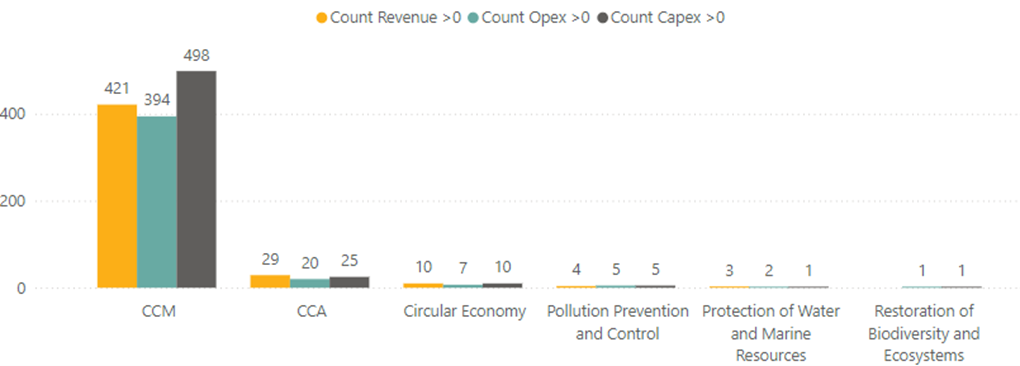

Analyzing the EU Taxonomy objectives that are reported on most by companies, we can see that climate change mitigation (CCM) remains the overwhelming focus. For 2023, out of 744 companies reporting on CCM, 498 reported above-zero alignment.

By contrast, of the 575 companies reporting on climate change adaptation (CCA), only 29 reported alignment above zero. CCA involves activities that help companies and communities adapt to the effects of climate change, such as extreme weather events, rising sea levels, or changing weather patterns. It is focused on resilience related to climate risks. These companies operate mainly in the consumer discretionary, industrials, and materials sectors.

Figure 5. Number of Companies Reporting Taxonomy Alignment per Objective

Source: Morningstar Sustainalytics. For informational purposes only.

Notes: Data from FY2023. CCM is climate change mitigation and CCA is climate change adaptation.

Meanwhile, even fewer companies have started reporting on alignment with the other four taxonomy objectives, namely circular economy, pollution, water, and biodiversity. This is partly because alignment reporting on these objectives is currently voluntary, but it will become mandatory from 2025 (i.e., for the 2024 financial year) in a phase-out way.

Low Reporting for Nuclear Energy and Natural Gas

This year, companies started reporting alignment to nuclear energy and natural gas. Following lively debates, the European Commission added these activities as sustainable energy sources in July 2022, significantly later than other sectors. These additions reflect a pragmatic approach to the transition toward a low-carbon economy while maintaining energy security.

The delayed inclusion of these two activities in the taxonomy means that companies have had less time to adapt their reporting framework to comply with the strict criteria, resulting in a slower uptake. Only 10 companies under our coverage reported above-zero alignment on nuclear energy activities and only one company reported on natural gas.

Reliability of Reported Data

It is still early days for taxonomy reporting and investors should be mindful of reported data inaccuracies, incompleteness, and misalignment. We found that 88% of companies either reported inaccurate data or left out one of the required datapoints. Morningstar Sustainalytics fill in the gaps where possible, based on available correct reported data. Meanwhile, 10% didn’t meet the “do no significant harm” (DNSH) or "comply with minimum safeguards" conditions for full taxonomy alignment. Addressing these discrepancies is essential for ensuring the credibility and integrity of sustainability reporting.

To learn more about the current state of EU taxonomy alignment in 2024, read the full report, EU Taxonomy Reporting Review.