What is Point of Sale Financing?

Point of sale financing (PSF) is a relatively new financial product that has garnered significant interest from consumers, retailers and financial institutions. It provides financing to markets that were previously underserviced by conventional financial products but can also be a gateway to impulsive spending and poor financial choices if not managed properly. This article provides a brief overview of PSF, the pros and cons for consumers, a comparison of PSF with conventional lending vehicles and a sector review looking at policies addressing financial inclusion.

PSF first emerged in Australia in 2014 and has since gained popularity in the UK and the US. It allows consumers to pay for purchases ranging from USD 10 to USD 5,000 over several weeks to a few years, as opposed to paying in full at the time of sale. Lenders review an applicant’s banking statements (such as monthly account inflows and outflows) instead of credit scores to determine creditworthiness within seconds. This allows applications to be made at the checkout where, if approved, borrowers will repay the outstanding total in instalments. For more information on PSF, Forbes and EY have in-depth explanations on how it all works.

Some of the frontrunners in the PSF market include fintech firms like Affirm, Afterpay and Klarna. Established payment companies, such as PayPal, American Express and JPMorgan Chase, along with US regional banks, such as Citizens Financial Group and Fifth Third Bancorp, have invested in this area via partnerships with companies that have established frameworks in the industry or by operating their own PSF services. Declining credit card use among millennials, the growth of e-commerce and advancements in payment technologies have fuelled interest in the past few years.

PSF: The Pros & Cons for Consumers

PSF can provide more convenience through flexible payment terms and options, as borrowers can choose terms that best suit their spending habits and needs. PSF’s approval processes increase access to financing for those who do not use credit cards, have poor or no credit history, or are underserved by traditional banking services, while interest rates are often lower than traditional credit cards or personal loans.

In addition, most companies currently offering PSF services state they limit payment penalties on loans and will not allow borrowers to continue using their service if the borrowers have any unpaid debts with the company; penalty fees generally account for a small portion of their revenue models.

Lastly, PSF allows consumers to make a purchase they otherwise might not be able to afford due to high upfront costs. Most retailers will pay for any fees associated with lending and disclose repayment schedules, helping consumers manage their finances more easily.

However, consumer advocates have criticized PSF’s quick approval processes for encouraging impulsive spending practices and poor financial choices. This is especially the case when multiple loans are taken out at the same time, which may cause some borrowers to lose track of the true cost of their purchases.

Retailers using PSF report higher average transaction values and increased sales figures, suggesting that consumers may be enticed to purchase more than they otherwise would if they had to pay for purchases upfront. Debts left unpaid on these platforms can also be sent to collection agencies, like other forms of debt, and may reflect negatively on an individual’s credit rating.

Since the loan underwriting process requires personal banking information to be reviewed, PSF also raises concerns over data privacy and security, as the information used to determine a consumer’s creditworthiness could be stolen or misused for malicious purposes.

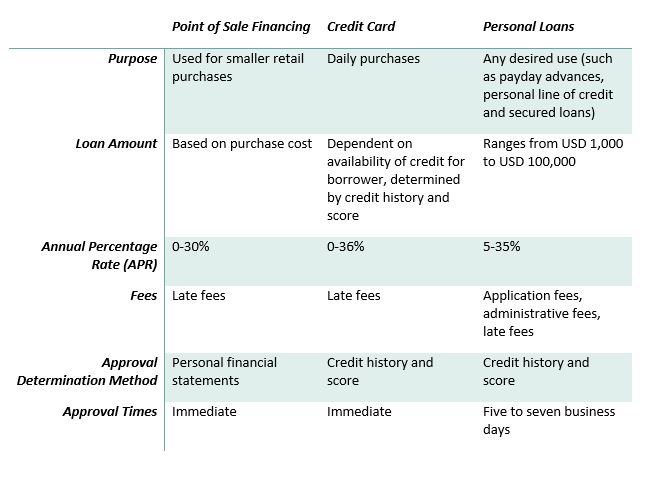

PSF vs. Other Forms of Credit

Sector Review

In an analysis of diversified financial companies covered in Sustainalytics’ rating universe, a subset of 300 companies in the sector was analyzed for financial inclusion performance (see graph below). The analysis reveals that just over half of companies sampled have some level of program in place, but less than 10% of those programs are considered strong. This indicates that there are significant opportunities for financial companies to mitigate the social concerns associated with their product offerings and to make their products financially accessible to a wider group of previously underserved consumers. As PSF becomes more widespread and companies begin to create their own PSF services, we expect the percentage of companies without financial inclusion programs to decrease in the coming years.

Financial Inclusion Indicator Performance (by percentage)

The Future for PSF

Over the next several years, if credit card usage rates remain low in the US market, PSF may become the norm as millennials face growing challenges in building their credit score and dealing with the high cost of living. In many Asian countries, the growing middle class, which is increasing demand for goods and services, combined with a high cost of living is anticipated to drive the adoption of PSF among retailers. Technological improvements have made digital banking and financial transactions easier to facilitate and to integrate into e-commerce, which is expected to help further PSF’s reach in the financial industry.

Conclusion

Ultimately, consumer demand for increased convenience, flexibility and technological advancements are projected to push all major retailers to offer PSF and for most financial institutions to develop an offering or partner with established fintech companies in this market. While PSF companies have demonstrated initiatives to mitigate the risk of predatory lending practices associated with credit cards and personal loans, social concerns over increasing debt loads are still a valid issue. The participation of major financial institutions like JPMorgan Chase and PayPal is likely to signal others to venture into this market, which may drive competition that can benefit consumers.