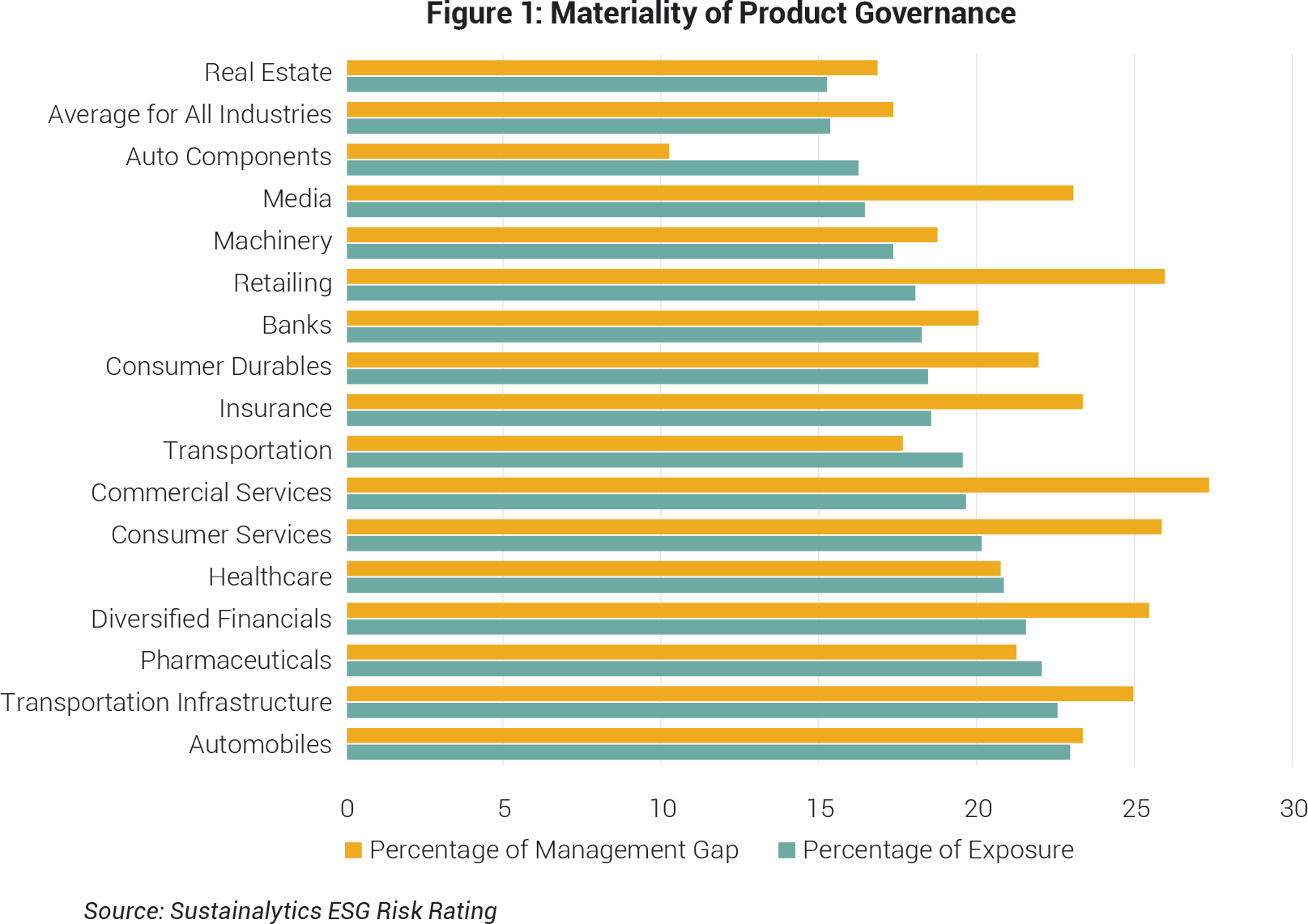

Sustainalytics’ Material Risk Engagement program engages with more than 320 companies in approximately 30 different industries worldwide. In 68% of our engagements, product governance is a significant material ESG issue, but it is our experience that most companies underestimate the materiality of this risk to investors. For some industries, product governance represents on average more than 20% of ESG risk exposure, as identified within our ESG Risk Rating framework. Moreover, as shown in figure 1, this issue represents even a larger portion of the management gap for almost all industries, reflecting relatively weak management of product governance risks. Product Governance remains one of the most undervalued ESG issues across industries despite the significant level of risk it presents to companies.

Product governance focuses on managing the risks to a company’s customers in using its products or services. Another product-related issue, E&S Impact of Products and Services, is about the social and environmental impacts of a company’s products and services. Product quality and safety are certainly important parts of product governance, but the impacts can be significant for many industries. Looking at financials for example, product governance focuses on responsible marketing and ensuring customer suitability to avoid misconduct including discriminatory lending practices, predatory lending, misleading investors through poor disclosure and illegal foreclosure practices.

- For automobiles, it includes the integrity and accuracy of companies’ product claims (including the marketing of safety performance and fuel economy levels) and the sales practices of companies’ financing services.

- For pharmaceuticals, it includes informing customers or responding to complaints about unanticipated side effects.

Considering the materiality of these issues, product governance should be a critical ESG disclosure consideration for companies. Poor management of product-related risks can have an immediate impact on sales and reputation and lead to massive fines.

Below we dive deeper into automotive and financial companies to share some insight from our engagements experience with companies in these sectors.

Automakers are Showing Progress

The “Dieselgate” scandal with Volkswagen that emerged in 2015 continues litigation and we have observed a negative impact on the brand. In 2020, Volkswagen admitted that the scandal had cost 31.3 billion euros in fines and settlements. The issue drove the automotive industry to review its practices for calculating fuel efficiency, resulting in more realistic and comparable measures for consumers.

We are engaging with 11 of the largest automakers in the world and are looking at product governance beyond fuel efficiency. The industry is under fierce competitive pressure combined with heightened expectations from regulators and consumers to decarbonize products and production. This is creating a focus on innovation, and companies are releasing new models at a fast pace. Combined with the growing technological complexity of the vehicles, this increases the risk for incidents related to product quality and safety.

Investors need to have a line of sight into companies’ performance in managing product quality and mitigating safety hazards. Still, until now, it has been the exception rather than the rule for automakers to disclose statistics on product incidents and recalls. Major incidents or recalls have often been disclosed in separate announcements, making it difficult to derive consistent insight into a company’s overall performance over an entire year.

Sustainalytics has engaged on these issues, and we have seen much better disclosure on product incidents and recalls from Hyundai and Kia. Both companies also recognize that product quality needs to improve to reduce product incidents and recalls, which have a directly associated cost and damage the customer experience and the brand overall.

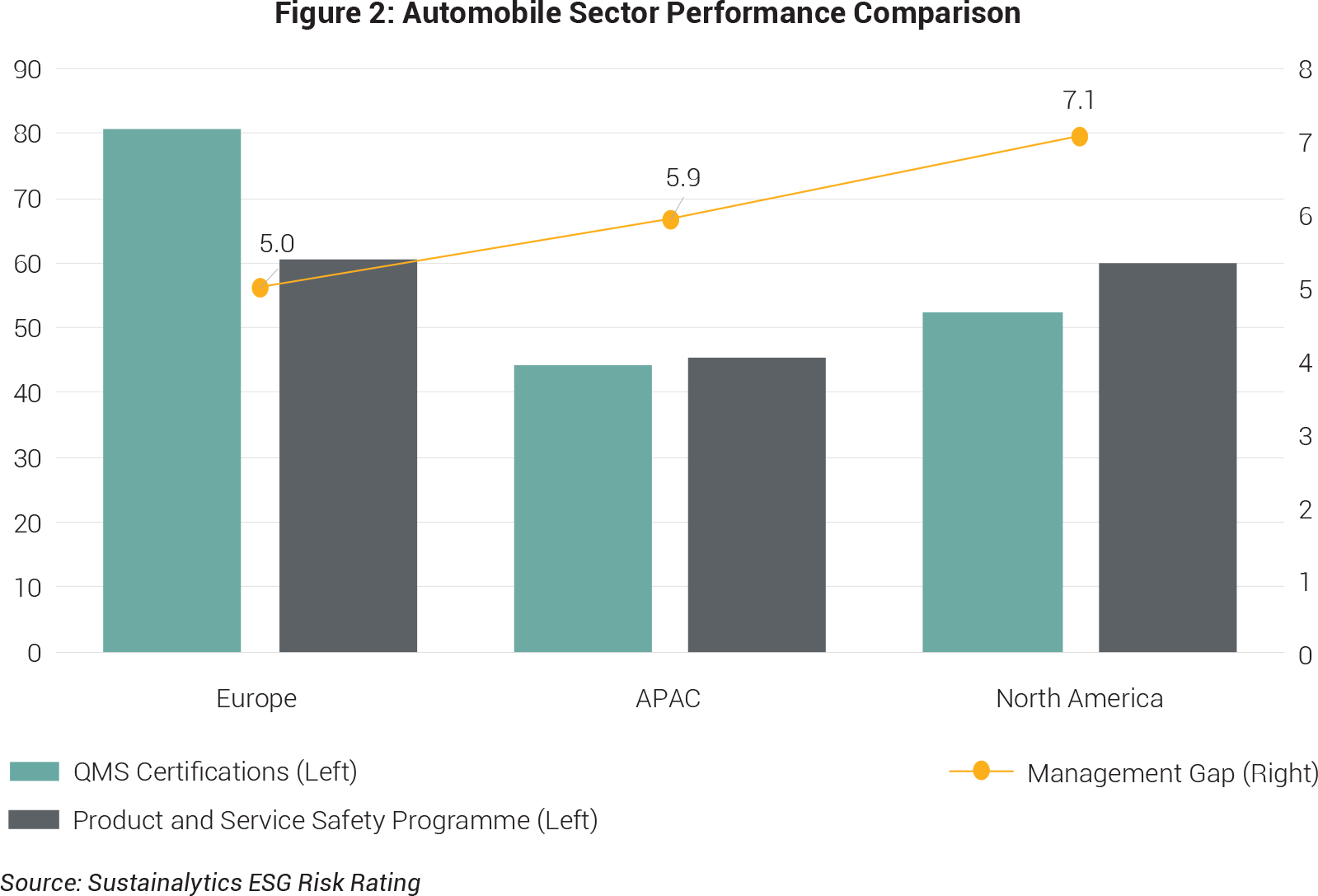

Our research shows that North American automobile companies have a higher management gap on product governance than in Europe and APAC (figure 2). Notice here that product-related incidents picked up in our research increase management gaps, so even if North America has better product and service safety programs than the APAC region, the management gap is on average higher. There is significant potential to engage on more consistent quality management practices and more cohesive product safety programmes.

Financials – Beyond Customer Experience

For financial companies, including banks, insurance and diversified financials, product governance goes beyond customer experience and satisfaction. Misconduct in marketing and customer suitability, such as discriminatory lending practices, predatory lending, misleading investors through poor disclosure and illegal foreclosure practices, has resulted in significant operational and reputational damages, as well as expensive fines.

For example, some of the world’s largest banks have been involved in customer-related investigations and lawsuits related to misrepresenting the risks of mortgage-backed securities, misleading IPO statements and charging inappropriate fees. The settlements of these investigations and lawsuits have cost banks billions. Credit Suisse has so far made legal settlements amounting to over USD $5 billion and faces further lawsuits, which could increase the legal and financial risks associated with a Mozambique bond offering controversy.

Best practices to manage these risks include:

- Having a clear governance structure to oversee responsible product offering matters,

- Conducting risk assessments of new products and services to verify that they fulfil the needs of consumers before they are launched,

- Continuous monitoring of social impact and risks of existing products and services, and

- Provide regular training of employees on responsible product offerings and marketing.

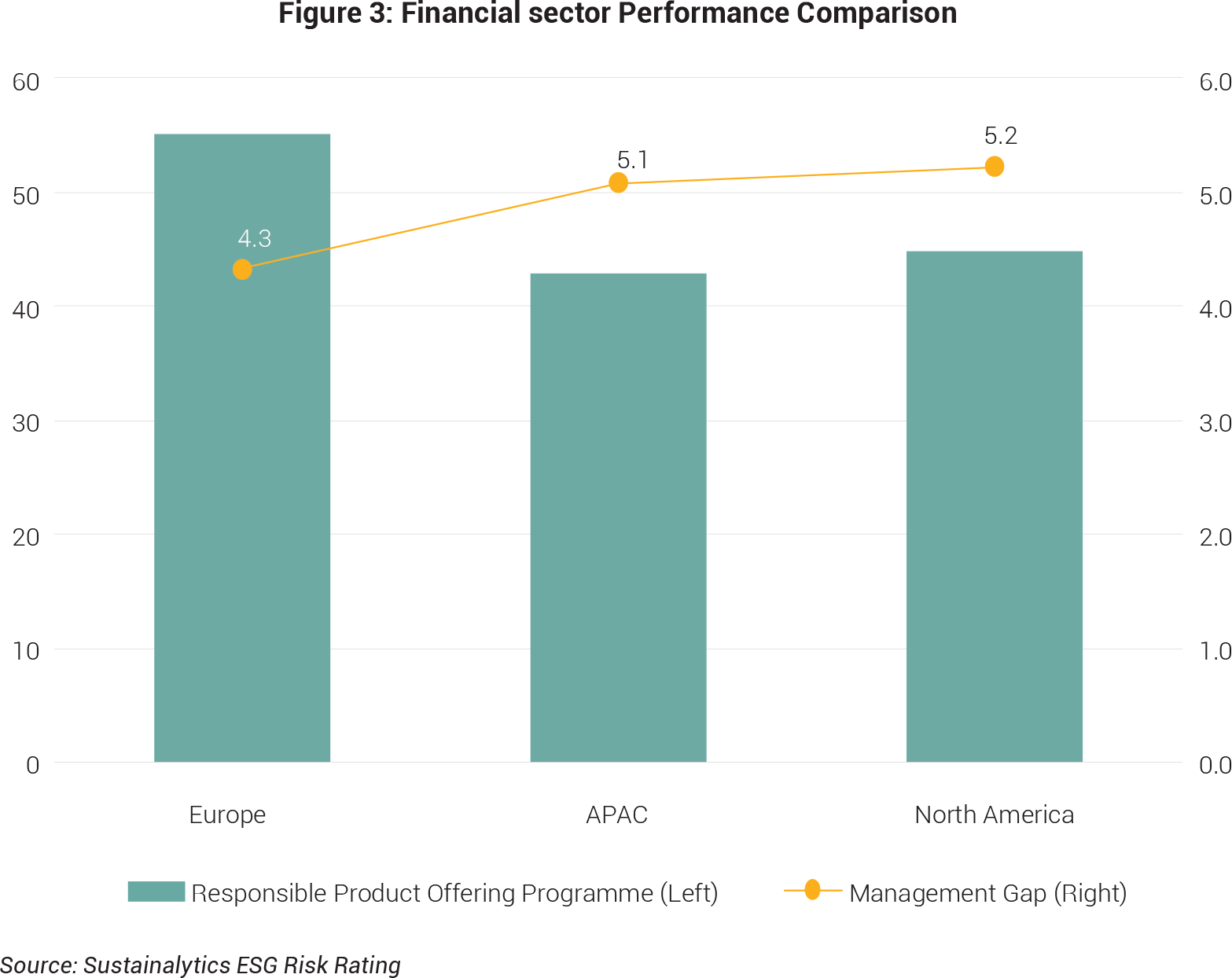

Our research (figure 3) finds that European financial companies historically tend to outperform North America and APAC on product governance, partly because they demonstrate stronger responsible product offering programs. However, APAC financial companies have recently been involved in fewer product quality controversies than their European and North American counterparts. This could be due to heavier financial regulations in many APAC countries.

From an engagement perspective, we work with financial companies to integrate ESG holistically into their operations, from risk assessment to product design and risk management. We encourage commercial banks to adopt the Principles for Responsible Banking initiative as a relevant reference point and network to adopt best practices. We encourage alignment and participation in the Principles for Responsible Investment for financial companies involved with asset management. Combined with ESG integration, financial companies need a robust code of conduct that addresses ethical issues related to products and customer management.

To see our latest Material Risk Engagement Report, you can email our team at mre@sustainalytics.com.

.png?Status=Master&sfvrsn=d51ed96e_1)