Globally, oil and gas companies are weathering a storm like no other in their history. Although volatility seems to have settled somewhat since the early months of 2020 (when the Russia-Saudi Arabia oil price war experienced its most heated moments yet), cost-cutting and debt borrowing continues to plague the industry as the vast majority of COVID-19 related restrictions remain in place worldwide.

In response to these hardships, government authorities – particularly those of Canada and the US, where oil sands and shale producers have been hit especially hard – have been quick to dish out support for the industry, whether through tax benefits or through helpful “amendments” to existing industry regulations and operating standards. While such actions are well-intentioned and focus both on curbing the spread of COVID-19 and preserving jobs across the industry, lowering the regulatory or legal bar on important ESG issues may also have the potential of doing more harm than good.

“Deregulation” across the North American oil and gas industry is aimed at decreasing costs and streamlining operations for companies.

In Canada, Alberta stands out as a jurisdiction that has taken significant steps to halt or reduce environmental regulations amidst the COVID-19 pandemic. However, other provinces such as Ontario, British Columbia, and Newfoundland and Labrador have also made similar decisions. Some examples of relevant changes for the oil and gas industry have included:

- Exclusions provided to offshore exploratory drilling projects in Newfoundland from being required to undergo project-specific federal environmental impact assessments.[1]

- Suspension of reporting requirements for companies operating oil and gas wells in Alberta relating to the condition of wells (this does not include reporting emergencies or regulatory contraventions).[2]

- Suspension of reporting requirements for oil sands companies in Alberta relating to volatile organic compounds (VOCs) releases, wetland monitoring, and fugitive emission leak detection and repair (LDAR) activities.[3]

- Postponement of carbon tax increases until further notice for companies in British Columbia. Alignment of carbon tax rates with the federal carbon pricing backstop methodology is also postponed until further notice. [4]

In the US, widespread loosening of environmental standards has been implemented through the US Environmental Protection Agency’s (EPA) Enforcement Discretion Policy. The policy addresses noncompliance with federal environmental permits, regulations and statutes that occur as a result of the COVID-19 pandemic. [5]Although the EPA has since issued a termination addendum which sets August 31, 2020 as the end date for the policy, increasingly concerning COVID-19 infection rates in several US states calls into question whether substantial reopening of local economies can (and should) occur and in extension, whether oil and gas producers will reasonably be able to return to regular operating conditions.

While these changes have been stated as only being temporary (although many do not currently have anticipated end dates), discontinuity of key standards and reporting requirements has the potential of negatively impacting the reliability of collected data, even over short periods. As a result, compliance and enforcement functions across the regulatory system can become impaired in the long-term.[6]

Existing commitments to the environment and society are potentially misaligned with taking advantage of temporary policy or regulatory cutbacks.

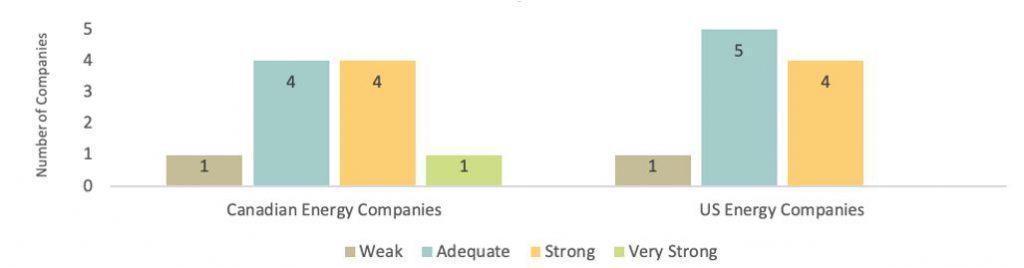

Based on our review of the policy commitments of 10 of the largest Canadian and US energy companies, it appears that most major players in the industry are committed to managing environmental issues at a level that is either adequate or strong. From our review, we found that most environmental policies include explicit commitments to environmental protection, using resources more efficiently, and monitoring and reporting on environmental issues. Relating to health and safety, virtually all companies had specific policies which committed to upholding the highest possible level of safety.

Exhibit 1: Environmental Policy Strength, Canadian and US Energy Companies

Source: Sustainalytics

While these findings do suggest a strong sense of accountability for ESG issues, choosing to leverage cutbacks on environmental or social requirements – although legally allowed – can represent a serious misalignment between stated commitments and actual management actions. Furthermore, on key issues like biodiversity and emissions management, underperformance has the potential of increasing ESG risk and contributing towards negative environmental and social outcomes.

Regulatory standards and protections are essential to avoid future global health emergencies and to protect social wellbeing.

Although “deregulation” across the oil and gas industry undoubtedly aims to serve a noble cause (i.e. the protection of individual health and the preservation of numerous jobs), the risk to ESG performance cannot be argued. As stated by David Boyd, the UN Special Rapporteur on Human Rights and the Environment, in his April 2020 address, amidst the COVID-19 pandemic, weakening or suspending environmental regulations will make things worse. Instead, there is even more of a need to accelerate efforts to achieve the 2030 Sustainable Development Goals (SDGs), given that a healthy environment is a cornerstone in preventing pandemics and protecting human rights.[7]

Sources:

[1] https://www.canada.ca/en/impact-assessment-agency/news/2020/06/the-government-of-canada-announces-new-regulatory-measure-to-improve-review-process-for-exploratory-drilling-projects-in-the-canada-newfoundland-an.html

[2] https://open.alberta.ca/publications/ministerial-order-219-2020-energy#summary

[3] https://www.aer.ca/documents/decisions/2020/20200429A.pdf#page=3

[4] https://www2.gov.bc.ca/assets/gov/taxes/sales-taxes/publications/notice-2020-002-covid-19-sales-tax-changes.pdf

[5] https://www.epa.gov/sites/production/files/2020-03/documents/oecamemooncovid19implications.pdf

[6] https://ablawg.ca/2020/05/07/covid-19-and-the-suspension-of-environmental-monitoring-in-the-oil-sands/

[7] https://www.ohchr.org/EN/NewsEvents/Pages/DisplayNews.aspx?NewsID=25794&LangID=E