The Russia-Ukraine conflict and the subsequent sanctions on Russian entities have led to material and wide-ranging impacts on diversified sectors and international firms. However, company disclosures and other sources suggest that the conflict’s primary impact on the global insurance industry is limited for two main reasons. First, global insurers have historically had a limited Russian presence, as the sector is dominated by domestic players. The top 10 firms (based on gross written premiums), commanding total market share of 82% as of 2020, are all domestically owned.[1] Second, per Morningstar data, the largest Russia and Ukraine exposure for a global insurer represents less than 3% of revenue and 5% of assets. Moreover, asset managers’ and owners’ direct Russia exposure is estimated to be minuscule. US insurers’ total direct investments in Russia were below USD 1.5 billion as of end-2021, which is negligible considering the industry’s total invested assets of more than USD 7.5

trillion.[2] However, it is likely that exit costs from Russia on the insurance companies may be higher than these levels, as Allianz already communicated a potential one-off hit of EUR 0.4 billion to EUR 0.5 billion.[3]

Still, the global insurance sector is not immune to the spillover effects of the Russia-Ukraine crisis, as should become apparent in the near future. Although international insurance companies have limited direct exposure to Russia and Ukraine, substantial insurance claims could arise as a result of physical and financial damage to clients’ property, such as stranded aviation assets, and business losses. Additionally, in line with heightened data security and cyberattack risks for global companies,[4] cyber insurance practices may change and the claims/loss risk on such products could rise precipitously. Moreover, property-casualty (P&C) insurers and diversified insurance companies are prone to relatively high litigation and reputational risks from a product governance perspective, and recent developments on the Russia-Ukraine front will add to the mix of challenges that insurers face.

How important is litigation risk?

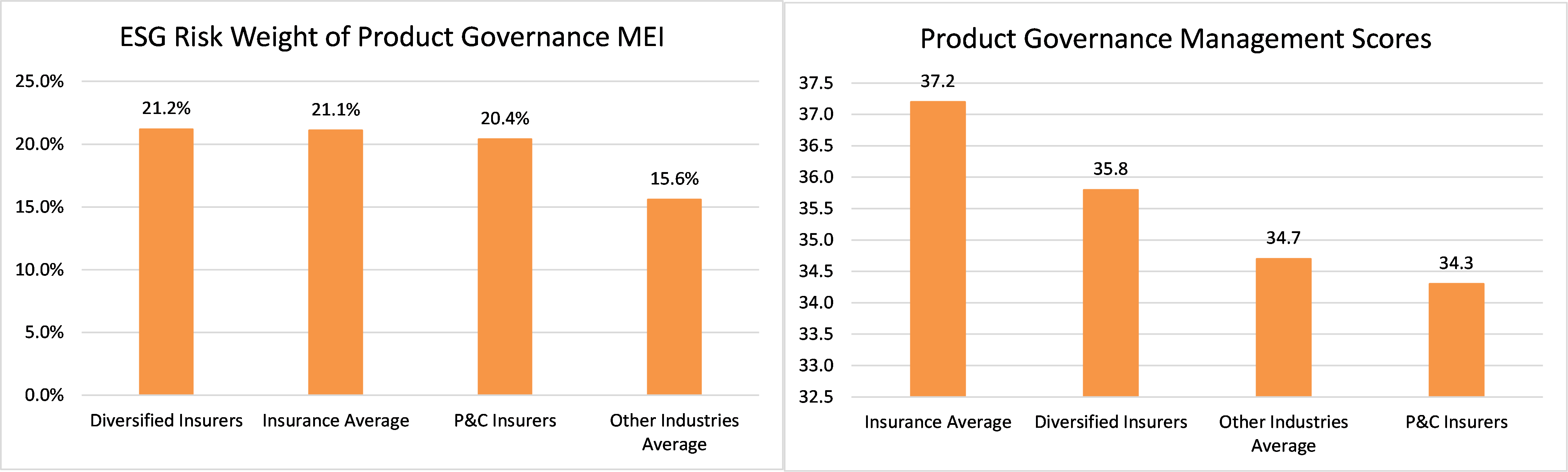

The spillover effects of the war will primarily be visible in insurance companies’ underwriting practices and in claims and litigation risk management. A deeper dive into the sector’s performance on the product governance material ESG issue (MEI) and granular controversies data helps us understand the ESG dynamics. The insurance sector has a sizeable ESG risk weight of 21.1% for the product governance MEI, with no significant deviations across its subindustries, versus an average of 15.6% for other sectors. Moreover, insurers’ average management score for this MEI is 37.4 (i.e., companies are managing 37.4% of the manageable risks), slightly better than the average of 34.7 for other sectors. However, diversified and P&C insurers exhibit slightly weaker performance on this metric, with respective scores of 35.8 and 34.3.

Figure 1: ESG risk weights and management scores for the product governance MEI

Source: Sustainalytics

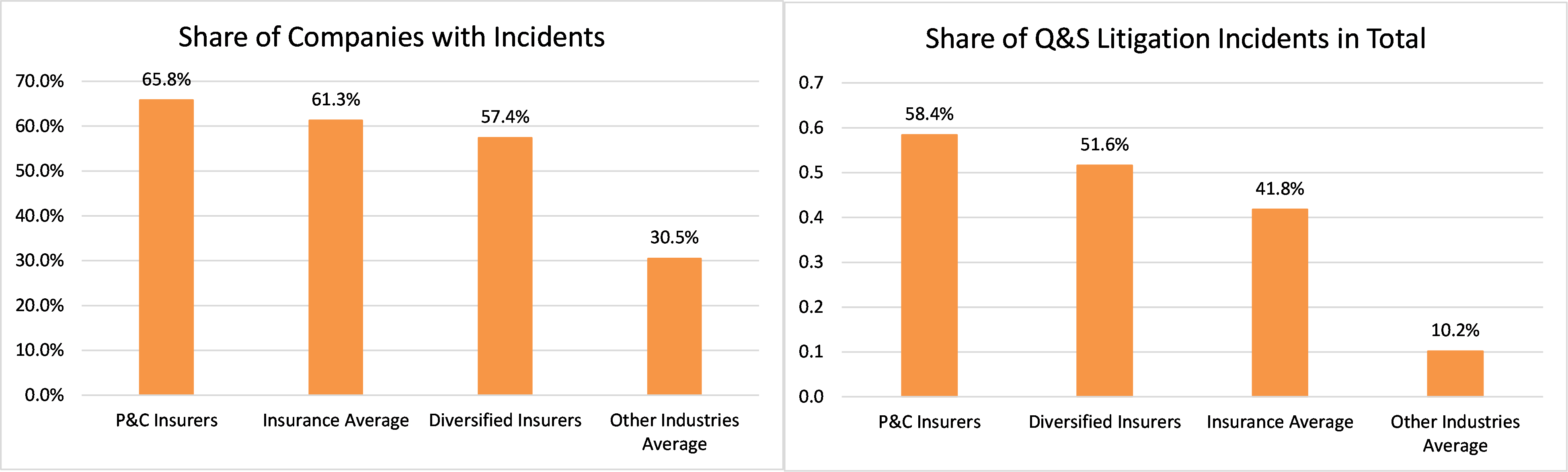

Owing mainly to the frequent disputes between policyholders and underwriters/intermediaries, insurance operations tend to be involved in more litigation incidents than other sectors (61% of insurers have incidents, versus an average of 31% for other sectors). The vast majority of these litigation-driven incidents are naturally related to product quality and safety (Q&S). The insurance industry has by far the highest share of Q&S litigation-related incidents at 42%, versus an average of 10% for other sectors. This figure is even higher for P&C (58%) and diversified (52%) insurers.

Figure 2: Insurers face far more litigation incidents than firms in other industries

Source: Sustainalytics

Two systemic events have tested the global economy in the past two years: COVID-19 and the Russia-Ukraine conflict. Economic weakness, especially caused by systemic events like these, may trigger widespread business interruptions and lead to massive losses. Since businesses typically seek to cover their losses through insurance claims, any pushback from insurers could spark an increase in lawsuits during economic downturns. Currently, events driven by Q&S litigation-related incidents have around a 7% dilution impact on the insurance industry’s product governance ESG risk rating, as opposed to an average of 10% for other industries. This shows that impact on ESG scores has so far been largely contained, despite the insurance sector’s higher litigious nature.

What could go wrong for insurers?

Despite soaring losses during the pandemic, the insurance industry has thus far managed to sail the waves in terms of litigation risk management. However, insurers could face a growing wave of lawsuits due to a deteriorating business environment, especially in certain industries, such as aviation. For instance, Willis Towers Watson estimates that P&C insurers could face insured losses up to USD 15 billion as a result of the conflict,[5] while Lloyd’s of London anticipates losses in the range of USD 1 billion–4 billion for its UK underwriters from their Russia-related aviation industry exposures.[6] As witnessed during the COVID-19 pandemic, supply chain disruption could further exacerbate and lead to additional business interruptions, which may result in claims and disputes with non-life insurers.[7] Although Q&S related lawsuits are quite common for non-life insurers, increasing frequency and fines & settlement amounts might trigger regulatory and reputational risks for the companies.

Another emerging risk for the insurance industry is cyber coverage, considering the Russia-specific warnings highlighted by the UK[8] and US[9] authorities. The cyber insurance market in the US is still small compared with other product lines, with only a 0.4% share of total premiums, according to a report from MarshMcLennan and Fox Rothschild. Increasing cybersecurity risk due to the Russia-Ukraine conflict may create noticeable losses for insurers in this segment, which is already operating at combined ratios in excess of 100%, implying no operational profit. Although demand for the product is likely to accelerate further, growing claims may exacerbate litigation risks in the short to medium term. One such example is the recent successful lawsuit from pharmaceutical major Merck, which was awarded USD 1.4 billion in damages related to the NotPetya malware.[10] Insurers are very likely to look for direct exclusionary clauses in their cyber insurance policies, such as exclusion of war.[11]

Systemic events such as the Russia-Ukraine conflict, coupled with negative economic cycles, worsen the risk environment for insurance companies on various levels: financial, legal, reputational and regulatory. Although Q&S-related litigation has so far had limited dilution impact on product governance management scores and overall ESG Risk Ratings, any weakening in the trends may trigger downgrades in event ratings and adversely affect risk rating scores. Thus, while global insurers may face only limited immediate impact from the Ukraine-Russia crisis, the difficulty of predicting the spillover effects could pose a significant headwind for the industry.

Get in touch with our Client Advisory team for any questions regarding how your investments may be affected by these risks.

Sources:

[1] https://assets.kpmg/content/dam/kpmg/ru/pdf/2021/07/ru-en-insurance-survey-2021.pdf

[2] https://content.naic.org/sites/default/files/capital-markets-asset-mix-ye-2020-final.pdf

[3] https://www.ft.com/content/4b01e406-2637-4a31-8558-56f0b8832fcc

[4] https://www.theactuary.com/news/2022/03/09/cyber-insurance-claims-spike-following-russia-ukraine-conflict

[5] https://www.wtwco.com/en-US/Insights/2022/04/insurance-marketplace-realities-2022-spring-update

[6] https://www.ft.com/content/e62df5f9-1716-4220-b583-91ba24d4cfb2

[7] https://www.propertycasualty360.com/2022/03/04/russian-attack-what-are-the-insurance-implications-414-218617/?slreturn=20220305131529

[8] https://www.ft.com/content/4ead59e6-260c-445d-850c-43f54c69bef9

[9] https://www.fincen.gov/sites/default/files/2022-03/FinCEN%20Alert%20Russian%20Sanctions%20Evasion%20FINAL%20508.pdf

[10] https://www.wsj.com/articles/insurers-want-to-avoid-covering-war-ukraine-hacks-put-that-to-the-test-11643279403?mod=article_inline

[11] https://www.reuters.com/business/munich-re-tightens-up-cyber-insurance-policies-exclude-war-2022-04-08/