Key Insights

|

|

|

My previous article on our Low Carbon Transition Rating (LCTR) explained how, “If all companies and countries in the world continue to operate similar to the over 8,000 companies assessed under the LCTR, global temperatures are likely to rise to 3.1 degrees Celsius over pre-industrial averages.” As we commemorate Earth Day, it’s time for both corporations and investors to reflect on their role in the current trajectory, and how we can change course by following those who lead by example.

The LCTR considers a management score of 50 to be neutral and anything below 45 as weak. But the best performing industries have a mean management score of around 45. Further, only about 10% of the companies we’ve assessed have strong management, with scores above 55 points. Containers and packaging (47.2), telecommunication services (46.4) and household products (45.9) are among the industries that have the highest average management scores. In this article, we take a closer look at these and other leading industries and delve into the best practices that have allowed them to emerge as leaders in managing their climate risk under the LCTR.

Best Practice One: Setting Reduction Targets for GHG Emissions

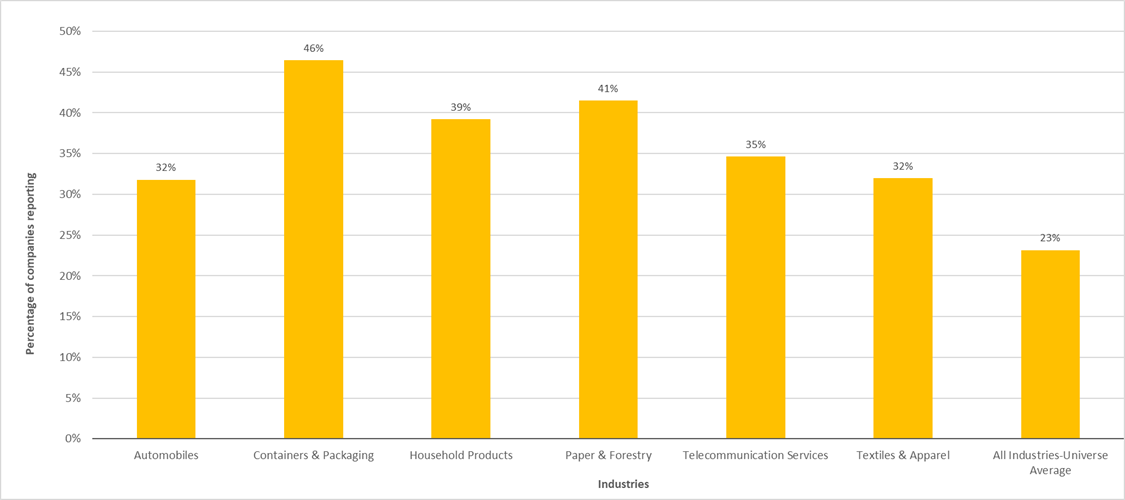

A focal point of the LCTR for assessing a company’s low carbon transition centers on whether a company sets a target to reduce its greenhouse gas (GHG) emissions and how robust these targets are. Just over a fifth of the companies we’ve assessed have set some kind of GHG emissions reduction target. Containers and packaging (46%), paper and forestry (41%), household products (39%), telecommunication services (35%), automobiles (32%), and textiles and apparel (32%) are among the top six industries in disclosing their GHG reduction targets (Figure 1).

Figure 1. Highest Reporting Industries on GHG Reduction Targets

Note: This analysis includes six industries due to automobiles and textiles and apparel being tied for the same level of disclosure.

Leading companies have high rates of setting absolute emissions reductions targets. A large proportion of these companies also have targets to reduce the GHG intensity of their emissions. There are a few companies in these industries which have only intensity-based targets, but they remain exceptions.

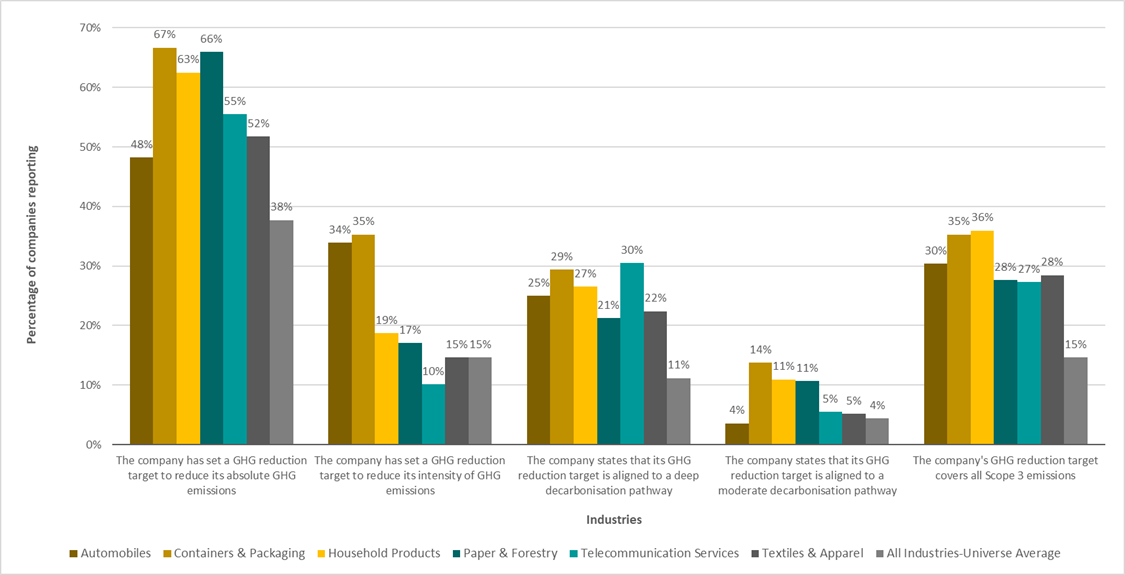

In most cases, leading companies and industries have GHG reduction targets aligned with either a deep decarbonization or a moderate decarbonization pathway; i.e., aligned to a 1.5 degree or 2 degree trajectory, respectively (see Figure 2). More companies are aligning their targets with deep decarbonization pathways and getting their targets verified through the Science Based Targets initiative (SBTi).

Figure 2. Performance Indicators for Highest Reporting Industries on GHG Reduction Targets

Source: Morningstar Sustainalytics. For informational purposes only.

In leading industries, we see a higher proportion of companies with verified science-based targets, particularly aligned to deep decarbonization and a move away from moderate decarbonization. Industries such as containers and packaging (46%), household products (33%), telecommunication services (28%), textiles and apparel (24%), and automobiles (32%) also have the highest proportion of companies with verified science-based targets.

One area where leading companies stand out is in setting and disclosing specific scope 3 emission reduction targets. Implementing scope 3 targets requires significant engagement with suppliers, as well as work towards reducing downstream product emissions – often through changing the products sold or substantially redesigning them. While only 15% of the companies assessed in the LCTR universe have specific scope 3 reduction targets, leading industries have about 30% of their companies setting scope 3 targets.

Best Practice Two: Linking Board and Executive Pay to GHG Reduction Targets

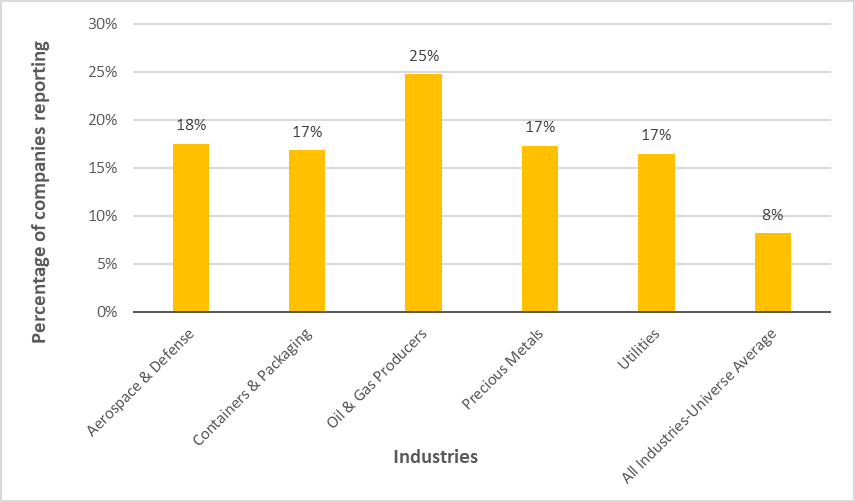

Across the entire LCTR universe, only about 8% of companies have some disclosure on the link between performance on GHG reductions against targets and senior decision maker incentives. Oil and gas companies are under increasing pressure to decarbonize their products and operations, transition away from fossil fuels and become providers of clean energy. In this context, it is unsurprising that they lead (25%) on linking decision makers’ incentives with progress against the company’s GHG reduction targets (see Figure 3 below). We also see other top performing industries such as aerospace and defense (18%) and containers and packaging (17%) leading on this indicator.

Figure 3. Highest Reporting Industries on GHG Performance Incentives for Executives

Source: Morningstar Sustainalytics. For informational purposes only.

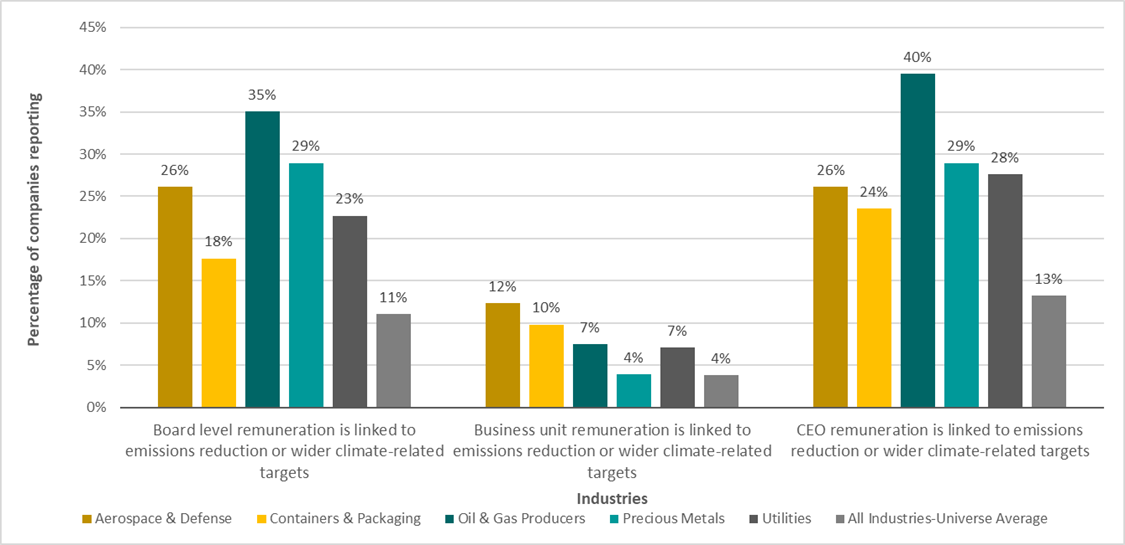

Most commonly, we see that a firm’s top decision makers such as the board and/or the CEO are the ones whose incentives are linked with achieving emissions reductions (Figure 4). But it is still uncommon to see these targets percolate down from the board to individual business units.

Figure 4. Performance Indicators of Highest Reporting Industries on GHG Performance Incentives for Executives

Source: Morningstar Sustainalytics. For informational purposes only.

Beyond setting targets, decision making centers in a company also need to have adequate understanding and resourcing to draft actionable transition plans. Over a quarter of the companies in the LCTR universe have a dedicated senior person with the responsibility to oversee emissions reduction efforts. A third of the companies have also appointed a board member who has some experience with business transformation or climate related matters. However, we see that only 3% of companies have provided the board with some form of training on the climate transition. While over 10% of boards claim to consult with internal and external stakeholders on matters related to climate and the transition that may affect the company or its stakeholders, the nature and details of these consultations remain vague.

Best Practice Three: Integrating Carbon Pricing

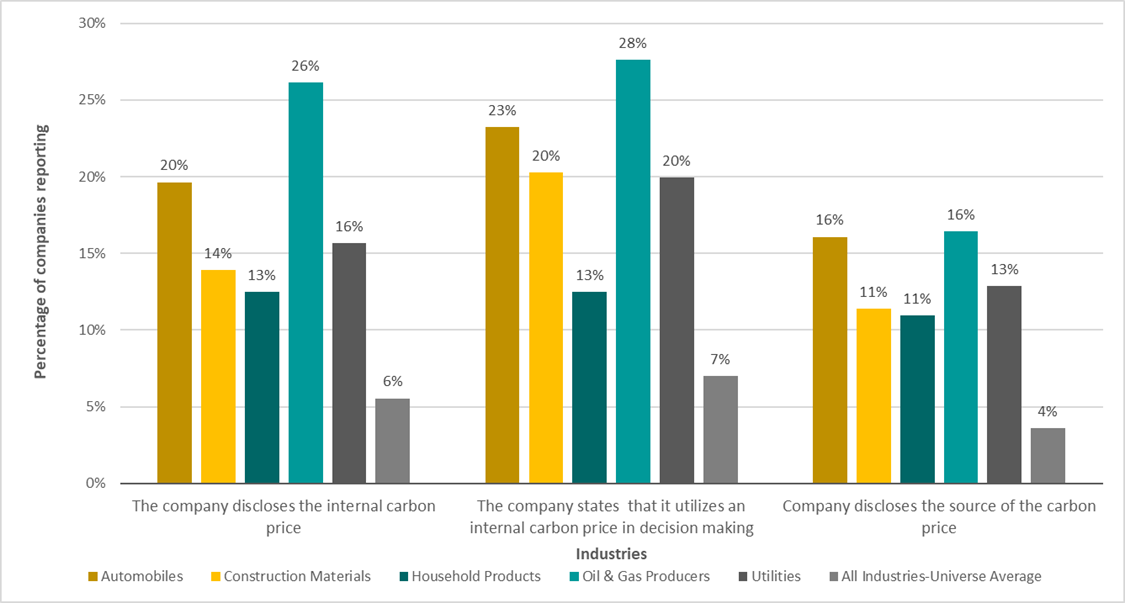

Another crucial element in ensuring that companies are adequately preparing for the low carbon transition is whether they use carbon pricing to make business decisions – especially ones that will have a longer-term implication for their business. It is important for businesses to anticipate future regulations such as a carbon tax or cap and trade market mechanism. Using internal/shadow/modeled carbon prices allows businesses to account for future cash outflows based on their emissions.

When it comes to instituting and reporting on integrated carbon pricing, high emitting and harder to abate industries tend to dominate the landscape. Oil and gas producers (28%), automobiles (23%), construction materials (20%) and utilities (20%) lead in stating that companies use an internal carbon price in decision making. There are not many commercially viable or scalable solutions available, but companies in these industries are doing well to incorporate carbon pricing into their decision making in anticipation of global price regimes for their products.

Figure 5. Highest Reporting Industries on Carbon Price Integration

Source: Morningstar Sustainalytics. For informational purposes only.

Best Practice Four: Setting Out a Long-Term Sustainable Finance Strategy

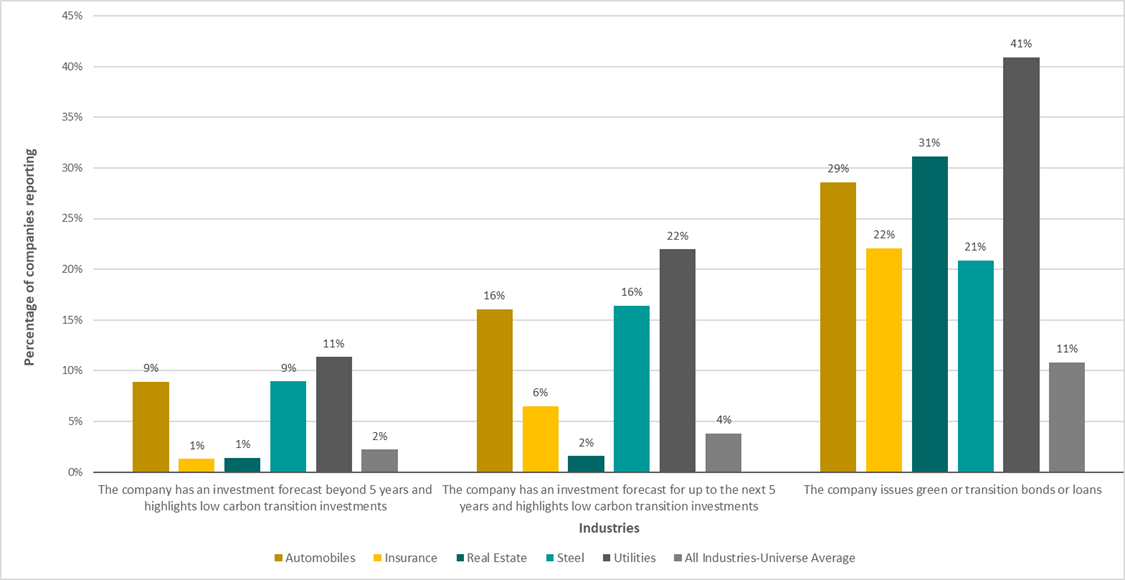

Among the companies assessed, over 10% have issued green bonds or loans to aid the investments required for greening their processes, infrastructure and products. Green bonds seem to be a more popular way to raise green capital amongst utilities (41%), real estate (31%), automobiles (29%), insurance (22%) and steel companies (21%) as seen in Figure 6.

Figure 6. Highest Reporting Industries on Low Carbon Transition Investment Planning

Source: Morningstar Sustainalytics. For informational purposes only.

Green bonds are a means for utilities to set up renewable energy capacities and real estate to help develop green and energy efficient buildings. Automobile companies seem to be largely utilizing green bonds to set up energy efficient manufacturing lines for zero and low emission vehicles. Steel companies are typically using green bonds to set up electric arc furnaces, and in some cases, pilot plants that reduce iron ore using hydrogen. The insurance sector is an outlier in this regard, as its focus is on issuing green bonds mainly to support the diversification of its investment portfolios.

Despite the popularity of green bond issuances, which typically mature after seven to eight years, there is fairly low disclosure on medium and long-term climate transition plans and forecasts, even among leaders. The only exceptions are with utilities, steel and automobiles. This seems to be driven by the fact that these industries are mostly directing their sustainable investments/green bond proceeds towards their own longer-term manufacturing (i.e., automobiles and steel) or economic infrastructure (i.e., utilities).

Best Practice Five: Green Technology Adoption

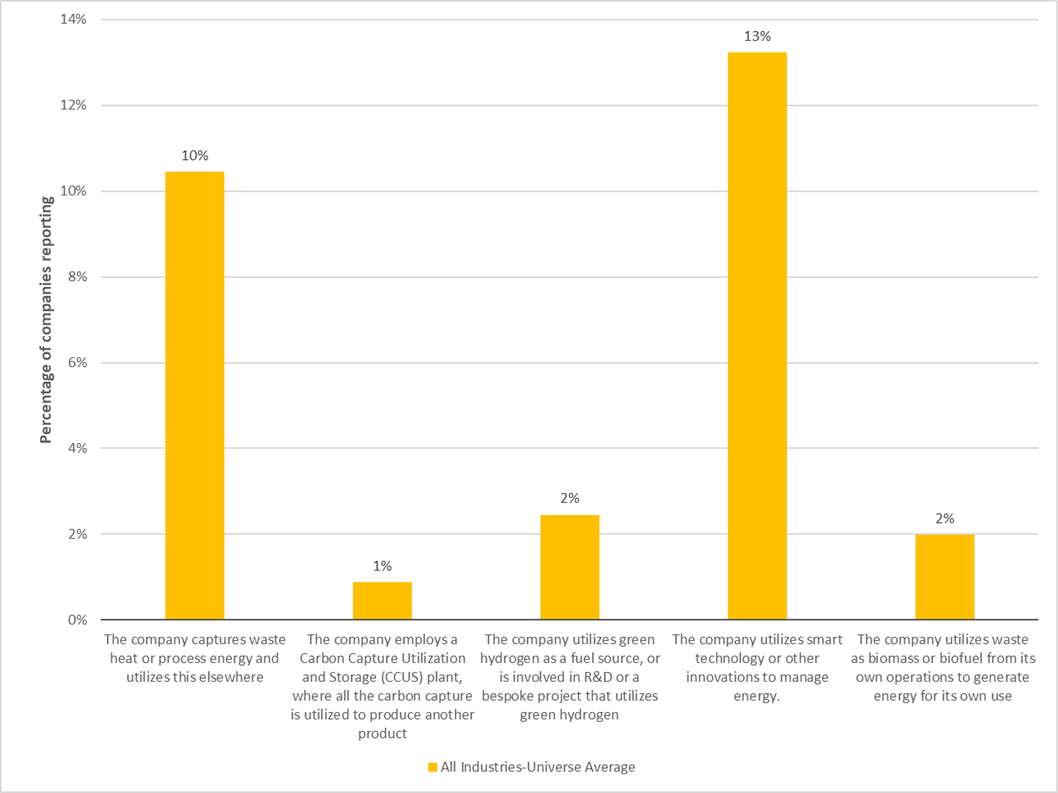

Across the LCTR universe of companies, we see that waste heat recovery and utilization (10%) and smart technology for energy savings (13%) are the most popular low carbon innovations being adopted (Figure 7). This is due in part to the scientific processes and technologies for these innovations being quite mature. The next most popular innovations are focused on the production of green hydrogen and setting up carbon capture, utilization and storage (CCUS) technologies. CCUS and green hydrogen are particularly popular among the oil and gas production as well as refiners and pipelines industries.

Figure 7. Universe Average Performance on Green Technology Adoption Indicators in the LCTR

Source: Morningstar Sustainalytics. For informational purposes only.

While green hydrogen is a top contender as a fuel to replace oil and gas, CCUS will help oil and gas companies to continue selling the same product while reducing the level of carbon being released into the atmosphere. Green hydrogen is also an innovation being targeted by nearly 10% of utilities, as it helps with energy needs such as heating and storing intermittent renewable energy.

Best Practice Six: Focusing on Supply Chain Emissions

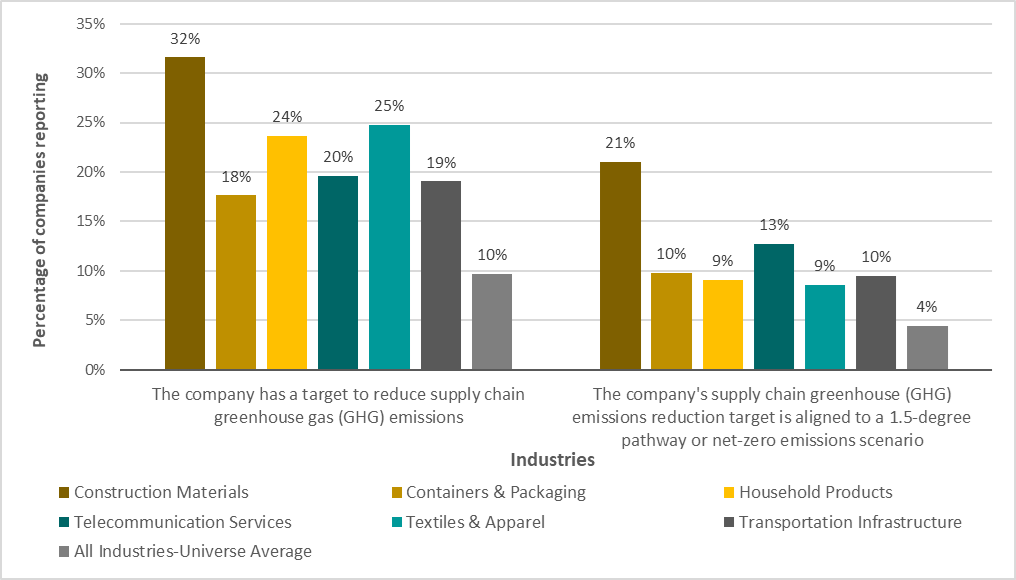

An important aspect of the LCTR is its focus on companies’ supply chain decarbonization plans. As with their own operations, this is centered around setting targets to reduce emissions from scope 3 emissions. For upstream emissions,1 the LCTR looks at targets set by companies to reduce their supply chain emissions. Industries such as construction materials (32%), textiles and apparel (25%), and household products (24%) continue their leadership in this area (see Figure 8). However, not all companies setting supply chain emissions reduction targets align them with the 1.5-degree goal. We see this even with the SBTi, where there are many companies which have scope 1 and 2 verified targets, but haven’t had their scope 3 targets verified.

Figure 8. Highest Reporting Industries on Supply Chain GHG Reduction Targets

Source: Morningstar Sustainalytics. For informational purposes only.

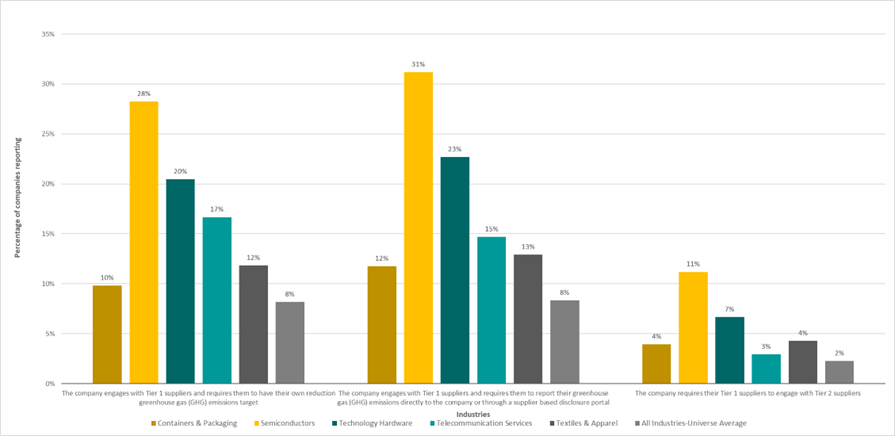

Beyond setting targets, we see that only 8% of companies engage their suppliers to set GHG reduction targets and report their GHG emissions directly to the companies (Figure 9). Also, only 2% of companies require their suppliers to engage with their own suppliers on emissions reductions. The industries leading on this all have large and complex supply chains, making having a supplier engagement program a necessity. These supplier engagement programs typically cover more than just emissions reductions and include other social and governance aspects as well. There are many companies (not scored for this indicator) which have supplier engagement programs, but do not specifically address GHG reductions.

Figure 9. Highest Reporting Industries on Supply Chain GHG Reduction Program

Source: Morningstar Sustainalytics. For informational purposes only.

The Need to Catch Up Now

The companies that consistently employ most of the best practices covered above form less than 10% of the universe of 8,000 assessed companies in the LCTR. They are largely concentrated in only a handful of industries. Many of these leading industries are not amongst the highest emitting industries. It is therefore imperative that all companies, particularly those in the highest emitting industries, reflect on these best practices and take action to manage the most crucial parts of their exposure to climate risks.

Learn how Sustainalytics’ Low Carbon Transition Ratings can help you assess transition risks within your portfolio. Contact our team or your client advisor.

References

- Upstream emissions are indirect GHG emissions related to purchased or acquired goods and services.