One of the lasting impacts of the COVID-19 pandemic will surely be a transformed understanding of supply chains. As we touched on in earlier posts[i] in our coronavirus blog mini-series, we expect the pandemic to catalyze a range of efforts by management teams to better understand the vulnerabilities of their supply chain. While executive teams closely track their tier 1 suppliers, many are unaware of the full scope of their global supply chain. Bain & Co recently estimated that up to 60% of executives have no knowledge of the items in their supply chain beyond the tier 1 level.[ii]

Supply chain excellence

With new emphasis on supply chains coming down the pipeline, it is important to recognize that some companies already have a head start. Sustainalytics’ Supply Chain Management indicator provides an insightful glimpse at corporate supply chain strategy. While it is not a perfect proxy for overall supply chain management, it captures many revealing elements, including board-level responsibility for supply chain issues, the use of supplier audits and mechanisms to monitor suppliers for non-compliant practices. Of the 2,560 companies that Sustainalytics currently evaluates on this indicator, only 37 (about 1%) receive our top assessment, including adidas AG, Intel, Kering, Nike and Telenor ASA.

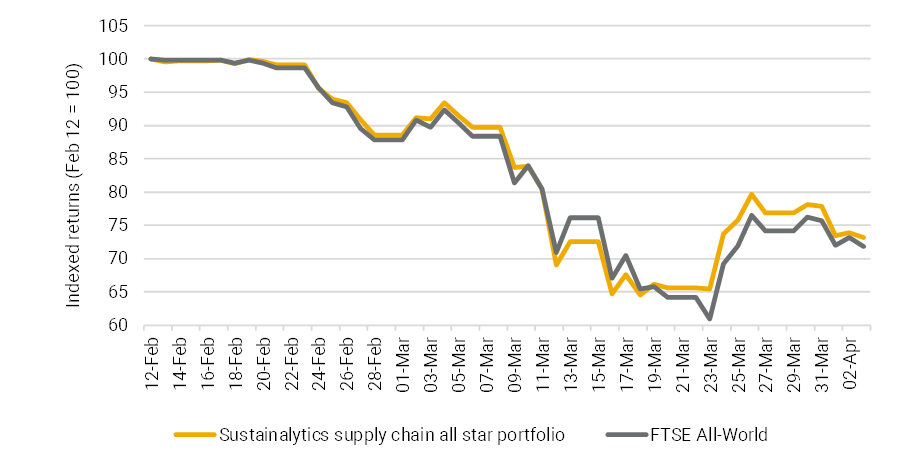

It has been postulated that one of the reasons ESG funds and indices held up relatively well during the COVID-19 sell-off is that they tend to be overweight companies with an effective grasp of their supply chain.[iii] To test this idea, we built an equal weighted model portfolio consisting of Sustainalytics’ 37 “supply chain all stars” and ran it against the FTSE All-World.

While the portfolio is illustrative, it provides initial evidence that companies with superior supply chain management practices may better hold their value in market downswings. As shown in Figure 1, the supply chain all star portfolio shed -27% from February 12, the high point for global equities, to market close on April 3, compared to -28% for the FTSE All-World. Clearly there are confounding variables to consider here, but we expect the idea that companies with superior supply chain management may also offer improved shareholder returns to be increasingly explored in the coming months.

FIGURE 1: SUSTAINALYTICS SUPPLY CHAIN ALL STAR MODEL PORTFOLIO VS FTSE ALL-WORLD

Source: Sustainalytics, Morningstar Direct

Small is beautiful?

Part of the re-assessment of supply chains that we see developing in the months to come includes renewed consideration of localized supply chains. Back in 1973 E.F. Schumacher wrote “Small is Beautiful”, in which he highlighted the benefits of more localized supply chains.

With the globalization of economies and markets across the world, it is not unusual for companies to depend upon low cost suppliers, including factories located in relatively cheap labour markets. But the shock of the coronavirus and the interruptions that many companies are feeling within these supply chains may cause companies to re-think this globalized supply market.

Often the model has been one of large production facilities producing large quantities of goods, with China often a preferred option. In 2003, when we had the SARS scare, China’s percentage of global GDP was 3 per cent: today it is closer to 20 per cent.[iv] So, when coronavirus struck in China and factories went into lockdown, the effect on the world’s supply chain was felt very shortly afterward.

For example, in a recent article,[v] the interruption to drug supplies in the US was highlighted as the supply from many of the plants manufacturing active pharmaceutical initiatives, which are based in India and China, have been interrupted. The interruption has been due to either local manufacturing being interrupted or the re-distribution of supplies to fight the pandemic locally rather than their export overseas. Similarly, who realised before COVID-19, that the vast majority of the world’s face masks were manufactured in China?[vi]

The issue of supply chain disruption is not a new one. As a 2014 article[vii] highlighted, a number of events had previously impacted global supply chains, including the 2011 tsunami in Japan (car manufacturing), the 2011 floods in Thailand (semi-conductors), and the 2010 volcanic eruption in Iceland (time sensitive supplies to and from Europe). But none have come close to the COVID-19 pandemic that is now sweeping the world.

While localized supply chains would likely increase manufacturing costs and prices for consumers, they could also bring material benefits in several areas. For example, they could lead to an increase in local jobs and tax revenues for governments. The carbon footprint of goods would be reduced, as components would not have to travel such great distances. Tighter supply networks could also lead to better enforcement of supplier standards and enhanced product quality.

Localized supply chains would clearly require a rethink in the dominant corporate model of seeking low cost suppliers, but we believe the COVID-19 pandemic has illustrated many of the weaknesses of this model that have been historically downplayed. And a diverse regionalized supply chain would better protect against regional or global disruptions in the future.

There will always be a need for certain commodities to be transported globally. Governments, for instance, often have a stockpile of strategically important commodities such as oil and uranium.

But overall, more localized supply chains, especially in vital good industries such as pharmaceuticals, could provide security for governments and companies, environmental benefits, improved product quality and increase resilience in times of global uncertainty.

As E.F Schumacher stated, “Small is Beautiful” and perhaps COVID-19 has simply helped to reiterate the point.

Sources:

[i] https://www.sustainalytics.com/esg-blog/coronavirus-oil-prices-and-esg-three-takeaways-for-investors/

[ii] https://www.ft.com/content/be05b46a-5fa9-11ea-b0ab-339c2307bcd4

[iii] https://grist.org/energy/as-coronavirus-infects-markets-sustainable-funds-prove-their-mettle/

[iv] https://www.supplychaindigital.com/supply-chain-management/covid-19-global-supply-chains-expect-major-reshuffle

[v] http://theconversation.com/medical-supply-chains-are-fragile-in-the-best-of-times-and-covid-19-will-test-their-strength-133688

[vi] https://www.businessinsider.com/covid-19-disrupting-global-supply-chains-how-companies-can-react-2020-3#larger-companies-can-build-regional-supply-chains-1

[vii] https://sloanreview.mit.edu/article/reducing-the-risk-of-supply-chain-disruptions/