International norms and standards centered on actual and potential adverse impacts, such as the OECD Guidelines for Multinational Enterprises (OECD MNE Guidelines) and United Nations Guiding Principles on Business and Human Rights (UNGPs), have played a progressively important role in the compliance and regulatory landscape, for both companies and investors.1 I explored the influence of actual and potential adverse impacts on businesses in greater detail in my previous blog.

In this blog I outline how investors with access to portfolio screening options that follow the criteria of the OECD MNE Guidelines and the UNGPs can better assess investee companies’ risk of causing actual and potential adverse impacts. I show what these research modules can look like and provide some examples of outcomes on the effect of applying certain thresholds.

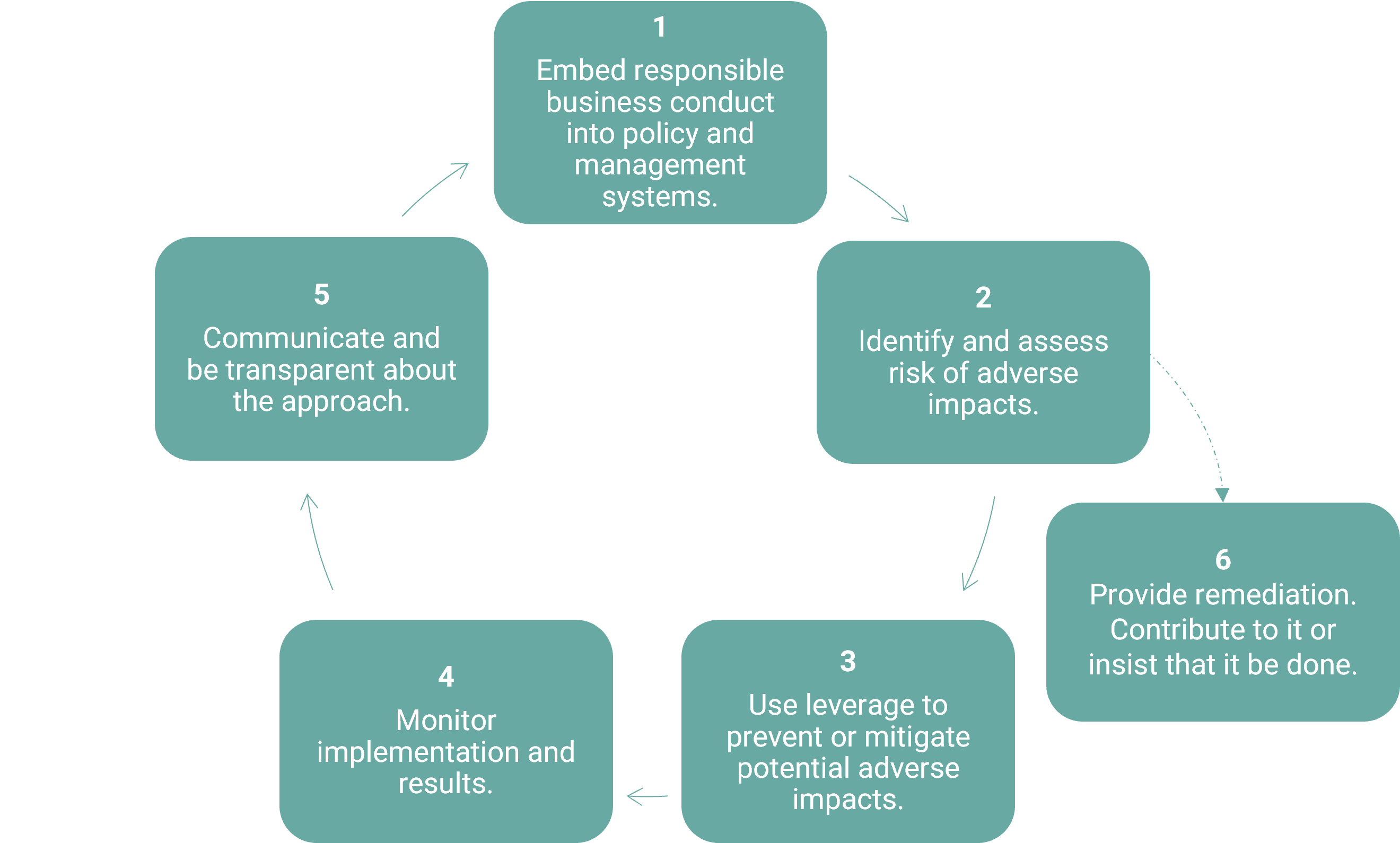

Steps to Achieving Responsible Business Conduct

For the implementation of these standards into investors’ due diligence, the OECD has provided support in its Guidelines for Responsible Business Conduct (RBC Guide).2 The concept of due diligence is key to understanding the requirements of the OECD MNE Guidelines and the UNGPs – investors should identify, prevent, mitigate, remediate, and account for how they address the actual and potential adverse impacts caused by investee companies in their portfolios.

The due diligence process outlined in the RBC Guide is a cyclical process, including clear steps that are suitable for implementation in institutional investors’ policy and management systems (Figure 1).

Figure 1: The Due Diligence Process for Responsible Business Conduct

Source: OECD RBC Guide

In line with this process, the first question that investors should be asking is: What are actual and potential adverse impacts, and how can these be identified? The RBC Guide encourages investors to apply a risk-based due diligence approach which could consider the following factors:3

- Risks related to the investee company’s sector and the nature of its activities.

- Risks related to the home country of investee companies and the country or countries of their operations.

- Risks related directly to the investee companies (e.g., poor environmental, social and governance track record).

- Priority issues identified in the investor’s responsible business conduct policy.

Identifying Violations of International Norms and Standards

The UN Global Compact Principles are regarded a basic starting point for assessing companies’ negative impact on stakeholders and the extent to which a company causes, contributes, or is linked to violations of international norms and standards. Although the UN Global Compact Principles reference OECD MNE Guidelines and UNGP, the scope of UN Global Company Principles is limited to 10 broad issues that can be applied for a holistic assessment of a company's actual or potential adverse impacts.

An assessment based on these dimensions can be made to determine if a company’s operations are considered compliant. Companies with a "Watchlist" or "Non-Compliant" status, respectively, are breaching or are at risk of breaching international norms. They are therefore considered to be at high risk of causing or contributing to actual adverse impacts.

When screening for these criteria in a portfolio, a "Non-Compliant" status would typically lead to the exclusion of a company from the investor portfolio (Figure 2 below). For a company with a "Watchlist" status, an alternative approach could be considered by means of active ownership. Our next blog will dive into the considerations for applying active ownership through engagement and voting.

Figure 2: Example Portfolio Screening for Compliance With the UN Global Principles

Source: Morningstar Sustainalytics. Based on Sustainalytics’ standard research universe. For informational purposes only.

Identifying Incidents and Events With Adverse Impacts

Looking beyond the scope of UN Global Compact Principles, important OECD and UNGP topics such as child labor or forced labor that occur in an investee company’s supply chain are receiving increased attention from investors. These can additionally be identified and screened for, based on incidents, events and controversies that reflect negative environmental and/or social impacts of the company activity.

It is important to note that there are two recommended ways to approach the severity of events in a combined manner: the negative impact on stakeholders and the negative impact on the company (e.g., reputational risk). To assess an event, it is recommended to look at the underlying incidents from a holistic perspective based on the following factors:

- Impact: Negative impact that the incidents have caused to the environment and society.

- Risk: Business risk to the company as a result of the incidents.

- Management: A company’s management systems and response to incidents.

Assigning levels or severity categories can help provide a clear overview of your assessments regarding controversies (Figure 3).

Figure 3: Example Portfolio Screening for Controversies

Source: Morningstar Sustainalytics. Based on Sustainalytics’ standard research universe. For informational purposes only.

Identifying Risk Related to Activities

When identifying risks related to an investee company’s sector, it is crucial to understand what activities a company undertakes. Numerous activities can be considered high risk for causing actual or potential adverse impact. For example, tobacco products have an unquestionable negative impact on human health and there is no harm-free use of the product. Therefore, tobacco producers can be considered as causing actual adverse impacts.

Looking at involvement with palm oil, however, the impact is related to and dependent on the business practices of the producers rather than the product itself. Therefore, it can be considered as a potential adverse impact. Other examples of product involvement that can be considered as causing actual or potential negative impact are fossil fuels, weapons, predatory lending and pesticides.

To support investors in their considerations, product involvement research can provide details on how a company is involved in one or more areas, as well as the degree of its involvement. In the figures below, we can see an overview of the percentage of companies from our standard research universe that are involved with, respectively, tobacco (Figure 4), thermal coal extraction (Figure 5) and palm oil (Figure 6), as well as their level of involvement.

Figure 4: Example Portfolio Screening for Product Involvements in Tobacco

Source: Morningstar Sustainalytics. Based on Sustainalytics’ standard research universe. For informational purposes only.

Figure 5: Example Portfolio Screening for Product Involvements in Thermal Coal Extraction

Source: Morningstar Sustainalytics. Based on Sustainalytics’ standard research universe. For informational purposes only.

Figure 6: Example Portfolio Screening for Product Involvements in Palm Oil

Source: Morningstar Sustainalytics. Based on Sustainalytics’ standard research universe. For informational purposes only.

In addition to identifying adverse impacts through product involvement research, an ESG Risk Rating can also be applied to identify which material ESG issues a company is exposed to, and how it manages this exposure.

Prioritization Based on Severity of Actual and Potential Negative Impacts

A risk-based approach recognizes that investors may prioritize the most salient risks for their due diligence. Salience describes those issues that create the most risk to people (as opposed to the business itself) through the company’s activities or business relationships.4 Therefore, another element in the due diligence process is to prioritize based on severity. The significance or severity of an adverse impact is understood as a function of its scale, scope, and irremediable character.5

The RBC Guide does not specify how to conduct this prioritization. As there is no one-size-fits-all approach when it comes to UNGP/OECD-related due diligence, thresholds can be modified according to investment values or beneficiary preferences. If, for example, an investor chooses to focus primarily on identifying human rights and labor rights risks, it can apply criteria that reflect this focus.

Our advisors are well positioned to provide guidance on how to determine relevant research modules and suitable thresholds for investors who are looking to implement due diligence on adverse impacts in their investment process.

References

- For further background, see the previous blog of this series.

van de Laar, Bart. "Applying Business and Human Rights International Standards to Investor Due Diligence." September 15, 2022. Morningstar Sustainalytics. https://www.sustainalytics.com/esg-research/resource/investors-esg-blog/applying-human-rights-international-standards-to-investor-due-diligence. - OECD. Responsible business conduct for institutional investors: Key considerations for due diligence under the OECD Guidelines for Multinational Enterprises. 2017. http://mneguidelines.oecd.org/RBC-for-Institutional-Investors.pdf.

- Ibid. Page 26.

- Principles for Responsible Investment. European supervisory authorities: joint consultation papers, ESG disclosures. 2019. https://dwtyzx6upklss.cloudfront.net/Uploads/l/f/a/esassfdrrts_final_335372.pdf.

- OECD. Responsible business conduct for institutional investors: Key considerations for due diligence under the OECD Guidelines for Multinational Enterprises. 2017. http://mneguidelines.oecd.org/RBC-for-Institutional-Investors.pdf.