Key Insights:

|

|

|

In early 2024, China’s vehicle exports surpassed five million for the first time, marking a significant shift in the global automobile market.1,2 This milestone propels China to the forefront of automotive manufacturing and is further exemplified by China-based BYD Co.'s electric vehicle (EV) sales eclipsing those of U.S.-based Tesla's sales in the final quarter of 2023. With BYD selling 526,000 battery-only vehicles compared to Tesla’s 484,500, it’s clear that the landscape of automotive manufacturing is rapidly evolving.

These figures represent more than just commercial success – they reflect profound changes across the auto industry worldwide, influenced by advancements in technology, shifts in consumer preferences, and increasing regulatory pressures for sustainability. For investors, these developments signal crucial trends that could impact investment portfolios. Automakers’ ability to adapt and capitalize on these shifts is not just pivotal for their competitive edge, but also for their financial viability and environmental, social, and governance (ESG) performance.

In this article, we go beyond mere sales numbers to examine how automakers are navigating this transformation, highlighting their financial and ESG results and the implications for investment strategies.

The Auto Industry in Brief: China’s Production Dominance and Tesla’s Market Cap Rise

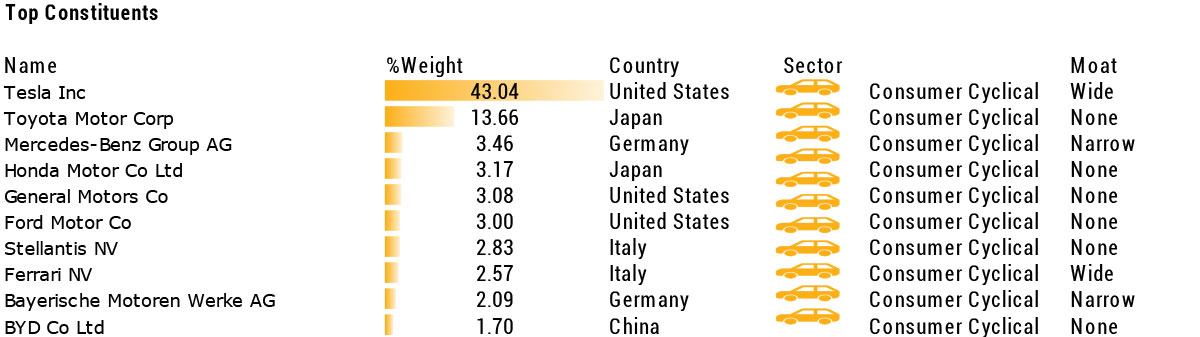

Worldwide, the automobile industry is divided between three big markets: the U.S., China, and the EU. The top 10 constituents of the Morningstar Global Auto Manufacturers GR USD Index (see Table 1) is a geographically diversified group. The total market cap of the index constituents approaches USD 1.5 trillion, highlighting its significant financial importance for investors. Tesla and Toyota are heavyweights in the index, with relative weights (market-cap based) of 43.04% and 13.66%, respectively. Three European companies are on the list: Mercedes-Benz, Ferrari, and BMW. BYD is the only Chinese company included among the top 10.

In terms of motor vehicle production, China ranks first, having produced about 27 million vehicles in 2022, the U.S. is second with production of 10 million vehicles, while Japan ranks third, producing about 7 million vehicles.3

Source: Morningstar. For informational purposes only.

In the U.S., the automobile market was previously dominated by the Big Three companies: Ford, General Motors, and Stellantis (formerly Fiat Chrysler Automobiles).4 In more recent years, Tesla has surged ahead in rankings, with a leading market capitalization of USD 663.1 billion (as of Jan. 25, 2024), about four times larger than the combined market capitalization of its Big Three competitors.5

The automobile industry continues to grow in China, with automakers such as SAIC Motor, China FAW Group, BAIC Motor, and Dongfeng Motor having emerged as the main domestic players.

Electric Vehicle Surge: Sales Soar Amidst Industry Shift Towards Sustainability

Automakers are paying more attention to ESG issues, particularly those related to the environment. The 2015 emissions scandal at Volkswagen resulted in overall increased scrutiny of the sector and tighter regulations on emissions reduction during vehicle use, including on carbon dioxide emissions. Furthermore, the EU and the state of California are moving toward allowing only electric vehicles for sale by 2035. In the U.K., a similar regulation will come into effect by 2030.

In this context, the much-anticipated EV segment has finally taken off over the past few years. Worldwide, EV sales jumped from USD 44.7 billion in 2016 to USD 561.4 billion in 2023.6 That figure is projected to nearly double by 2030. Meanwhile, the share of all new cars sold that are electric rose from 5% in 2020 to 14% in 2022, highlighting an acceleration of the transition toward electrification and cleaner fuel sources.7 A recent report published by the International Energy Agency (IEA) shows that in 2022, electric car sales surged by 55% in both the U.S. and China, and 15% in Europe.8 Lastly, as the transport sector contributes about 15% of total greenhouse gas (GHG) emissions, it can play a meaningful role in meeting the global objective of achieving net zero emissions and aligning with a 1.5-degree Celsius increase threshold established by the Paris Agreement.9

It is also worth noting that the development of EVs has been a discontinuous process, as companies are also weighing other options, including hybrid and solar vehicles.

ESG and Financial Performance: Divergent Trends in U.S. and Chinese Automakers

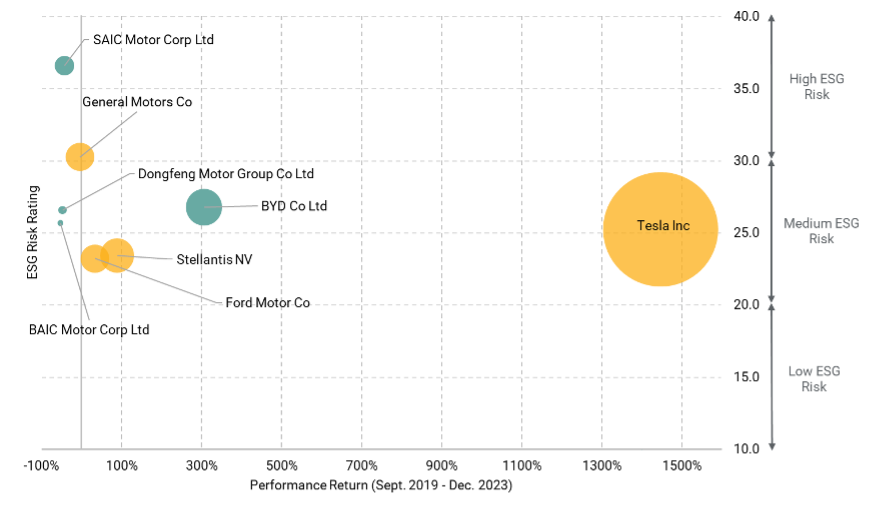

As investors increasingly prioritize ESG performance, it becomes important to explore the dynamic interplay between ESG and financial performance. Figure 1 depicts the financial performance (cumulative returns from January 2021 to December 2023) and the ESG Risk Ratings, as of January 2024, of the major U.S. and Chinese automakers. The size of the dots relates to the size of the companies’ market cap.

U.S. companies tend to have larger market capitalizations than their Chinese counterparts. Tesla is a standout with the largest market cap in the automotive industry (USD 663.1 billion as of January 25, 2024) and an astonishing cumulative return of 1,447.38% over the last three years. On the other hand, three of the four Chinese companies included in our sample had negative cumulative returns over the past three years, highlighting financial underperformance. Only BYD witnessed a significant positive return of 305.9%.

Looking at ESG performance, almost all the companies are in the medium ESG risk category, highlighting similarities in exposure and managing ESG-related challenges. Similar to the industry overall, exposure scores for these companies are in the medium category, signaling that there is no specific exposure gap between regions. Furthermore, how well these automakers manage the ESG risks to which they are exposed can translate into similar ESG Risk Rating categories for both pure-play EV makers, such as Tesla and BYD, and legacy automakers, as shown in Figure 1. The exceptions are SAIC Motor and General Motors, which display high ESG risk. We also find no clear divide between small and large companies in terms of ESG risk.

A closer look at the ESG Risk Rating scores also shows that Tesla performs slightly better in terms of exposure to and management of overall ESG issues than its Chinese peers, including pure-play EV maker BYD.

Additionally, no clear relationship emerges between financial performance and ESG risk. Perhaps the only stark differences are those between SAIC Motor and Tesla, as Tesla scores better on both financial and ESG risk.

In sum, the analysis shows that although Chinese automakers produce more vehicles and share, to some extent, comparable ESG risks with their U.S. counterparts, their market caps remain relatively small. In addition, Tesla’s price-to-book ratio in 2023 was equal to 14.77, while that of BYD was only equal to 4.48. The side-by-side comparison between Tesla and BYD, therefore, underscores a gap in market valuations and may offer opportunities for investors in search of undervalued assets.

Figure 1. Financial Performance and ESG Risk of U.S. and Chinese Automakers

Source: Morningstar Sustainalytics. For informational purposes only.

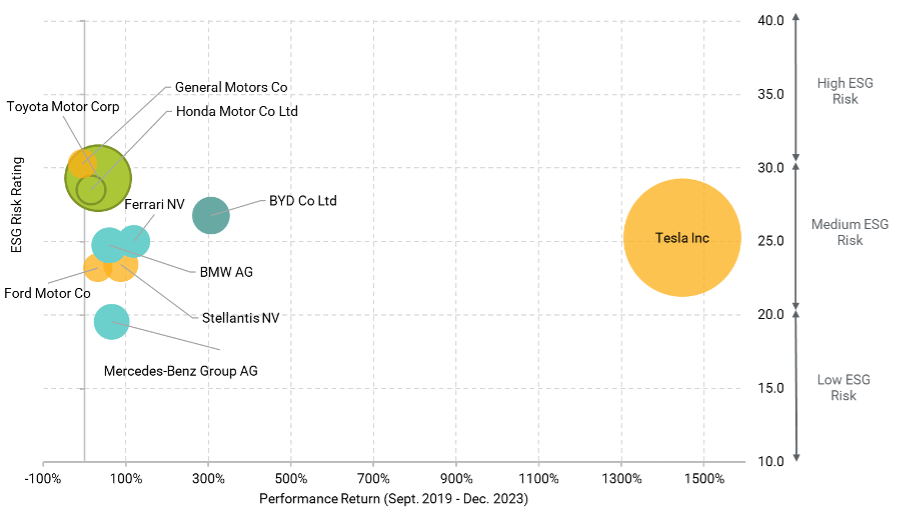

In Figure 2, we expand our analysis to the top 10 automakers globally (sorted by market cap), as reported in the Morningstar Global Auto Manufacturers GR USD index. Overall, the picture is similar to Figure 1. The cumulative return Jan. 2021 to Dec. 2023 is positive for all of these companies, except for General Motors (three-year return equal to -4.0%). Most automakers are in the medium ESG risk category. Mercedes-Benz, which has low ESG risk, is the only exception.

Figure 2. Financial Performance and ESG Risk of the 10 Largest Automakers Globally

Source: Morningstar Sustainalytics. For informational purposes only.

Navigating Change: Opportunities and Challenges in the Global Auto Industry Transformation

The profound shifts in the global automotive industry, marked by China's emerging leadership in vehicle exports and the competitive dynamics between leading EV manufacturers like BYD and Tesla, underline a pivotal period of transformation. This evolution is driven by rapid technological advancements, changing consumer demands, and stringent environmental regulations, presenting both challenges and opportunities for automakers and investors alike.

As the industry adapts to these changes, the financial stability and ESG performance of automakers will be critical indicators of their ability to sustain growth and profitability. Investors may want to focus on companies that demonstrate robust ESG frameworks and strategic agility in adapting to new technologies and regulations.

Furthermore, the ascendancy of Chinese automakers in the global market, especially in the electric vehicle sector, is reshaping competitive landscapes. For investors, this signals a need to reassess market positioning and potential growth areas, particularly where gaps in market valuations may offer opportunities for investors in search of undervalued assets.

By aligning investment strategies with the evolving landscape of the automotive industry, investors can not only manage risks more effectively, but also capitalize on the growth trajectory of pioneering companies within this space.

References

- The author would like to thank Clark Barr, Alex Osborne-Saponja, Driss Lembachar, Alina Olaru, Trevor David, Curtis File, and Alison Gray for their comments on earlier drafts of this report and Victor Ursulescu for the data analysis.

- Wayland, M. 2024. “Why China poses a growing threat to the U.S. auto industry.” CNBC. January 23, 2024. https://www.cnbc.com/2024/01/22/china-poses-growing-threat-to-us-auto-industry.html

- Wikipedia. Last modified 2024. "List of Countries by Motor Vehicle Production." Accessed May 28, 2024. https://en.wikipedia.org/wiki/List_of_countries_by_motor_vehicle_production.

- Stellantis is technically an Italian automaker, but we include it here as Chrysler was one of the big three companies in the US.

- Companies Market Cap. “Largest Automakers by Market Cap." Accessed May 28, 2024. https://companiesmarketcap.com/automakers/largest-automakers-by-market-cap/

- Statista. "Electric Vehicles Worldwide." Accessed May 28, 2024. https://www.statista.com/outlook/mmo/electric-vehicles/worldwide#revenue.

- International Energy Agency. 2023. "Global EV Outlook 2023: Catching up with Climate Ambitions." April 2023. https://iea.blob.core.windows.net/assets/dacf14d2-eabc-498a-8263-9f97fd5dc327/GEVO2023.pdf

- Ibid.

- Ritchie H., Rosado, P., and Roser., M. 2024. “Breakdown of Carbon Dioxide, Methane, and Nitrous Oxide Emissions by Sector.” Our World In Data. January 2024. https://ourworldindata.org/emissions-by-sector