The legal and regulatory foundations of Germany’s corporate governance system are being overhauled in the form of far-reaching changes to the German Stock Corporations Act (AktG) and the German Corporate Governance Code (Kodex). As a result, institutional investors should expect enhanced transparency from German issuers, as well as stronger rights enabling them to effectively exercise their stewardship responsibilities. The reform reflects both the transposition of the EU Shareholder Rights Directive II (SRD II) into domestic law and a corresponding Kodex revamp, both aiming to incorporate governance features that are more typically associated with Anglophone jurisdictions.

This blog post provides investors with an overview of the key changes to the German corporate governance framework.

Changes to corporate law

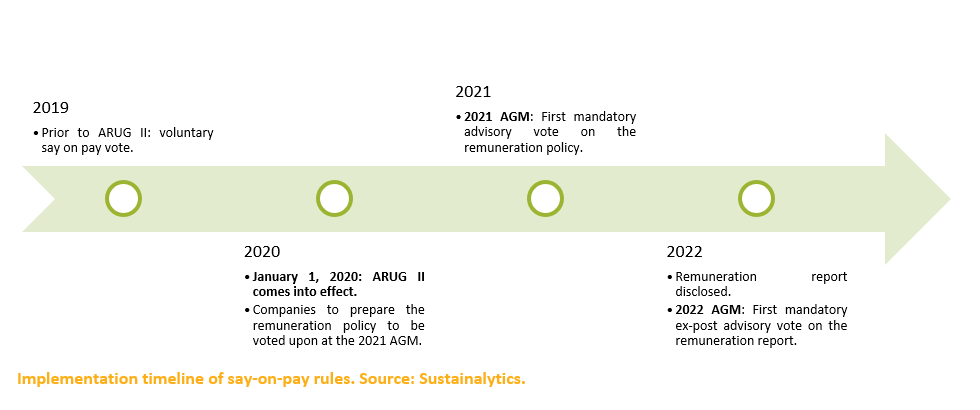

The European Parliament and the European Council adopted the SRD II in 2017 to “encourage long-term shareholder engagement” and tackle the shortcomings exposed by the 2008 financial crisis. Being a directive, EU member states retain a degree of discretion in transposing it into national law. The directive was transposed in German law in November 2019 and came into effect on January 1, 2020.

Say on pay

Under the new rules, companies are required to:

- submit the remuneration policy for an advisory vote at least every four years and whenever material changes occur[1].

- submit a revised policy for approval at the next annual general meeting (AGM)[2], should the above resolution fail to gain majority support[3].

In addition, the revised rules grant shareholders the power to request that the maximum remuneration for the executive board is reduced[4].

Related party transactions

Prior to SRD II, German companies were not subject to disclosure or approval requirements for related party transactions (RPTs)[5]. As of January 1, 2020, all material[6] RPTs require the approval of the board[7] or a board committee – the key difference being that any interested directors are to abstain from voting only if the full board approves the transaction[8]. Various exemptions are provided in this respect, most notably in cases where the company determines that the transaction is carried out in the ordinary course of business and under normal market conditions. To this end, companies are to set up an internal review process to assess the appropriateness of RPTs[9]. Per the new regulations, RPTs are also subject to extensive disclosure requirements, which include the obligation to make public any RPTs requiring approval within four business days[10].

These changes to German law will provide institutional investors a tool to voice dissatisfaction with the company’s compensation, with the enhanced transparency on RPTs allowing for a more comprehensive evaluation of a company’s governance.

Changes to the German Corporate Governance Code

The German Corporate Governance Code contains a set of non-binding best practice recommendations concerning the management and oversight of German listed companies, with the latter legally bound to annually report on their adherence to the Code’s provisions. The first edition of the Kodex was adopted in February 2002 and last amended in February 2017, with the SRD II having prompted the need to revise the Kodex once again to harmonize it with the new corporate governance framework. Accordingly, the 2020 Kodex was submitted to the Federal Ministry of Justice and Consumer Protection for review and will come into effect once published in the Federal Gazette.

Supervisory board independence

The Kodex first introduces specified board independence targets, which had been notably absent from past editions of the Kodex. Germany has often come under scrutiny for its perceived lack of board independence, partially attributable to the presence of founders and other major shareholders[11]. While Germany’s concentrated ownership structures are not unique compared to its European neighbors, its lack of an explicit minimum board independence is[12].

The 2020 Kodex also introduces:

- the recommendation that a majority of the shareholder-elected directors[13] of non-controlled companies be independent from the company and management board.

- a lower independence quota for controlled companies – with the independent directors to be independent from the controlling shareholder, as well[14],[15].

- criteria negating director independence: i) previous service on the management board without a two-year cooling-off period, ii) “material business relationships”, iii) “close” family relationships with a management board member, and iv) board tenure exceeding 12 years[16],[17].

Remuneration

The 2020 Kodex recommends that:

- long-term incentives constitute a majority of variable pay[18]

- the performance criteria related to pay be mainly assessed against strategic goals.[19]

- management board members not be entitled to any severance upon termination arising from a change in control[20].

- supervisory board remuneration be fixed, with any potential performance-related remuneration “geared to the long-term development of the company.”

These Kodex changes will enhance the disclosure requirements faced by German issuers, thus helping investors in their voting decisions and facilitating a more effective dialogue with companies.

As illustrated in this blog post, the German corporate governance system’s overhaul entails a direct and immediate impact on investors and issuers alike. Put into perspective however, the reform is evocative of a more structural shift in the global corporate governance landscape: the convergence of corporate governance models worldwide, fueled by globalization. Now, it remains to be seen whether the ongoing reform will translate in meaningful improvements to board composition, remuneration and accountability.

[1] § 120a I AktG

[2] § 120a III AktG

[3] Per § 120a V AktG, small and medium-sized enterprises (as defined in in § 267 HGB) are exempt from these requirements if the remuneration report is presented at the AGM for discussion.

[4] Adding an item on the AGM agenda is required for this. German law allows shareholders holding 5% or more of the company’s voting rights or shares with a value of at least EUR 500,000 to place items on the meeting agenda (§ 122 II Aktg

[5] The International Accounting Standard IAS24 defines related party transactions as transactions and outstanding balances between a reporting entity and a related party, regardless of whether a price is charged.

[6] According to § 111b I AktG, an RPT is deemed “material” if, alone or together with other transactions conducted with the same related party within the most recent fiscal year, it amounts to 1.5% or more of the total assets per the most recent annual financial statements.

[7] Throughout this article, the term “board” refers to either i) the supervisory board, in case of a two-tier board structure, or ii) the board of directors, in case of a monistic Societas Europaea (“SE”) board.

[8] § 111b II AktG and § 107 III AktG.

[9] § 111a II AktG.

[10] § 111c I AktG.

[11] Ringe, G. (2015). Changing Law and Ownership Patterns in Germany: Corporate Governance and the Erosion of Deutschland AG. American Journal of Comparative Law, 63(2), 493-538.

[12] Section 5.4.2 of the GCGC 2017 recommends that the board “include what it considers to be an appropriate number of independent members, thereby taking into account the shareholder structure.”

[13] Directors other than employee representatives appointed according to German Co-determination laws.

[14] Per recommendation C.9 of the 2020 Kodex, in the case of controlled companies with the board comprising more than six members, at least two shareholder representatives should be independent from the controlling shareholder.

[15] We do, however, highlight that most jurisdictions require that independent directors be independent from significant shareholders as well, with the threshold of “significant” shareholder varying from market to market.

[16] Recommendation C.7 of the 2020 Kodex.

[17] Per Recommendation C.8 of the 2020 Kodex , the company retains the autonomy to classify a director as independent in spite of one or more of these criteria, provided that the rationale is disclosed.

[18] Recommendation G.6 of the 2020 Kodex.

[19] Recommendation G.7 of the 2020 Kodex.

[20] Recommendation G.14 of the 2020 Kodex.

Sources:

- 2020 German Corporate Governance Code (Deutscher Corporate Governance Kodex 2020, “Kodex”)

- Act Implementing the Second Shareholder Rights Directive (Gesetz zur Umsetzung der zweiten Aktionärsrechterichtlinie)

- German Stock Corporation Act (Aktiengesetz, “AktG”)

- Directive (EU) 2017/828 of the European Parliament and of the Council of 17 May 2017 amending Directive 2007/36/EC as regards the encouragement of long-term shareholder engagement

- Franks, Julian and Colin Mayer (2017). Evolution of Ownership and Control Around the World: The Changing Face of Capitalism. ECGI Working Paper 503/2017

- Ringe, G. (2015). Changing Law and Ownership Patterns in Germany: Corporate Governance and the Erosion of Deutschland AG. American Journal of Comparative Law, 63(2), 493-538

- Gesetz über die Drittelbeteiligung der Arbeitnehmer im Aufsichtsrat (Drittelbeteiligungsgesetz, “DrittelbG”)

- Gesetz über die Mitbestimmung der Arbeitnehmer (Mitbestimmungsgesetz, “MitbestG”)

- Epstein, Marc J. “Challenges of governing globally: a strong understanding of the three distinct corporate governance systems around the world will help managers conduct business more effectively in other ”Strategic Finance, July 2012.

- Organisation for Economic Co-operation and Development (2019). OECD Corporate Governance Factbook 2019.

- The German Commercial Code (Handelsgesetzbuch, “HBG”)